Required minimum distributions sound simple — take money out of your retirement account once you reach a certain age. In practice, RMDs are one of the most complicated and costly areas of retirement planning.

Once you reach a certain age, the IRS requires you to start withdrawing from most retirement accounts on a fixed schedule, whether you need the income or not. These mandatory withdrawals are called required minimum distributions, and missing one can trigger a 25% penalty on top of your regular income taxes.

CFP® certificant Robin Sherwood compiled this guide that covers which accounts are affected, when distributions begin, how to calculate your annual amount, and how to avoid the mistakes that cost retirees the most.

Table of Contents

- What Is a Required Minimum Distribution (RMD)?

- Which Retirement Accounts Have Required Minimum Distributions?

- When Do Required Minimum Distributions Begin?

- How Are Required Minimum Distributions Calculated?

- Why Multiple Accounts Make RMDs More Complicated

- The Still-Working Exception to RMD Rules

- Required Minimum Distributions for Inherited Accounts

- The Cost of Getting RMDs Wrong

- RMDs as a Tax and Retirement Planning Issue

- Frequently Asked Questions About Required Minimum Distributions

- Work With a CFP® on Your RMD Strategy

1. What Is a Required Minimum Distribution (RMD)?

A required minimum distribution (RMD) is the minimum amount the IRS requires you to withdraw each year from most tax-deferred retirement accounts, starting at a specified age.

The logic behind the rule is straightforward: when you contributed to a traditional IRA or 401(k), you received a tax deduction. That money has never been taxed. RMDs are the IRS’s mechanism for ensuring it eventually is — by forcing withdrawals that are taxed as ordinary income.

2. Which Retirement Accounts Have Required Minimum Distributions?

Not all retirement accounts are subject to RMD rules — and that distinction matters, especially if you’ve accumulated savings across multiple account types over the years.

Accounts subject to required minimum distributions include:

- Traditional IRAs

- SEP IRAs

- SIMPLE IRAs

- Employer-sponsored plans: 401(k), 403(b), 457(b), and profit-sharing plans

Accounts exempt from lifetime RMDs:

- Roth IRAs (no lifetime RMDs for the original owner)

- Designated Roth accounts in employer plans (Roth 401(k), Roth 403(b)) — exempt from lifetime RMDs under current rules

The Roth exemption creates a meaningful planning opportunity. Because Roth IRA owners are never required to draw down their accounts during their lifetime, those assets can continue to grow tax-free for decades or be passed to heirs. For retirees with both pre-tax and Roth accounts, understanding which accounts trigger RMD requirements is the critical first step.

⚠️ Many retirees assume all retirement accounts follow the same distribution rules. They don’t. The first challenge is simply identifying which of your accounts are subject to required minimum distributions — and which are not.

3. When Do Required Minimum Distributions Begin?

The age at which you must begin taking required minimum distributions depends on when you were born.

Your first RMD is generally due by April 1 of the year following the year you reach your applicable starting age. Every subsequent annual RMD is due by December 31.

The First-Year Delay Trap

Delaying your first required minimum distribution until April 1 may seem harmless — but it means taking two taxable distributions in the same calendar year: the delayed first-year RMD and the current-year RMD. That double withdrawal can push your taxable income significantly higher, potentially affecting:

- Your federal income tax bracket

- Medicare Part B and Part D premium surcharges (IRMAA)

- The taxable portion of your Social Security benefits

The decision to delay or take your first RMD on time is not just an administrative choice — it’s a tax-timing decision that deserves careful consideration.

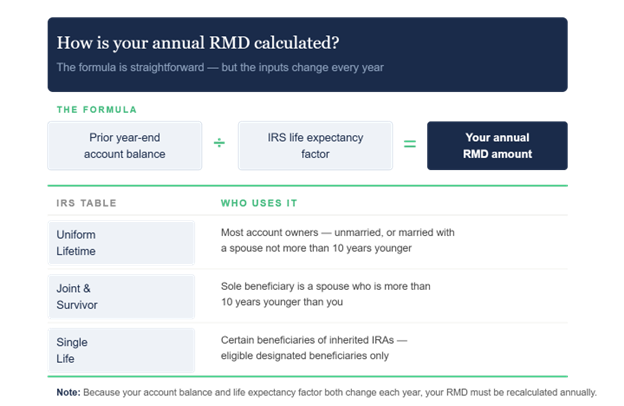

4. How Are Required Minimum Distributions Calculated?

Each year’s RMD is calculated using a straightforward formula:

Prior year-end account balance ÷ IRS life expectancy factor = Annual RMD

But the inputs change every year, and the wrong life expectancy table can produce the wrong result. The IRS provides three tables — which one applies to you depends on your situation.

Because the divisor changes each year as you age — and because account balances fluctuate — your required minimum distribution amount must be recalculated every year. You cannot simply repeat last year’s amount. Failing to recalculate is one of the most common — and most expensive — RMD errors.

💡 Key reminder: The account balance used for your RMD calculation is your balance as of December 31 of the prior year. Market gains or losses during the current year do not affect the current year’s RMD.

5. Why Multiple Accounts Make Required Minimum Distributions More Complicated

The complexity of required minimum distributions grows quickly when you have more than one retirement account. The aggregation rules — which govern whether you can combine RMDs across accounts or must satisfy each one separately — are not consistent across account types.

IRA Aggregation Rules

If you own multiple IRAs, you must calculate the RMD for each IRA separately. However, you may take the combined total from any one or more of your IRAs in any combination. This gives you flexibility in choosing which accounts to draw from.

Each spouse’s IRAs are treated independently — you cannot combine your IRAs with those of your spouse to satisfy either person’s RMD obligation.

Employer Plan Rules

Employer-sponsored plans — such as 401(k) plans — generally do not allow aggregation. If you have two 401(k) accounts, you must satisfy the RMD from each plan individually. You cannot take a larger distribution from one plan to cover the other.

Exception: 403(b) accounts may be aggregated for RMD purposes, similar to IRAs.

A Common Multi-Account Scenario

Consider Carol, who retired last year with four accounts: a rollover IRA, a SEP IRA from her years of self-employment, and two old 401(k)s from former employers.

For her IRAs, Carol can calculate each RMD separately and pull the combined total from whichever account she prefers. But each 401(k) must be satisfied on its own — she can’t take a larger distribution from one to cover the other.

That means four accounts, three custodians, and two different sets of rules to track every year. Miss a distribution from even one account, and she faces a significant penalty on the shortfall — with no flexibility to make it up from the others.

6. The Still-Working Exception to Required Minimum Distribution Rules

Age alone doesn’t determine when required minimum distributions must begin. Employment status matters too.

Participants in certain employer retirement plans may be able to defer RMDs until they actually retire — even past their applicable starting age — if the plan allows it. This is sometimes called the “still-working exception.”

Important limitations:

- This exception applies only to the employer plan where you are still actively employed.

- It does not apply to IRAs — IRA RMDs must begin at your applicable age regardless of employment status.

- It does not apply if you are a 5% or greater owner of the business sponsoring the plan.

- It does not apply to old employer plans at companies where you are no longer employed.

As a result, two people of the same age can face very different RMD obligations depending on whether they’re still working, what type of plan they have, and their ownership stake in the company. This is where coordination between account types becomes critical.

7. Required Minimum Distributions for Inherited Accounts

Inheriting a retirement account comes with its own set of distribution rules — and they vary significantly based on your relationship to the original owner, when they died, and the type of account. Most non-spouse beneficiaries must fully distribute the account within 10 years, though certain beneficiaries — such as surviving spouses, minor children, and disabled individuals — may qualify for more favorable treatment.

One aggregation rule worth noting: inherited accounts can only be aggregated with accounts inherited from the same decedent. For example, an IRA inherited from your mother cannot be combined with one inherited from your father.

For a full breakdown of beneficiary categories, the 10-year rule, and special rules for inherited Roth accounts, see our blog: Inherited IRA Distribution Rules: What Beneficiaries Must Know.

8. The Cost of Getting Required Minimum Distributions Wrong

Missing or underpaying a required minimum distribution is one of the most penalized mistakes in retirement planning.

The additional tax: Failing to take your full RMD can trigger a tax on the shortfall. The penalty was reduced from 50% to 25% under SECURE 2.0, and may be further reduced to 10% if the error is corrected promptly. But even at the lower rate, the penalty is significant — and the tax on the distribution still applies.

Multiple custodians create blind spots: If you have accounts at more than one financial institution, no single custodian necessarily sees the complete picture. Your IRA custodian may calculate your IRA RMD correctly, while your former employer’s plan administrator separately calculates a workplace plan RMD that cannot be offset by the IRA withdrawal. Each account type must be handled independently.

Automatic withdrawals are not a guarantee: Even when custodians provide RMD estimates or set up automatic distributions, the account owner is ultimately responsible for confirming that the correct amount was withdrawn from the correct account. Relying entirely on automated systems without verification is a common source of errors.

9. Required Minimum Distributions as a Tax and Retirement Planning Issue

RMD compliance is only one part of the equation. From a planning perspective, required minimum distributions can reshape your entire retirement income picture.

How RMDs Affect Your Tax Situation

- RMDs from traditional IRAs and employer plans are taxed as ordinary income.

- A higher RMD can push you into a higher federal income tax bracket.

- Increased income can trigger Medicare IRMAA surcharges (1–2 year look-back period).

- More income can cause a greater portion of your Social Security benefits to be taxed.

Planning Strategies That Interact With RMDs

- Roth conversions: Converting pre-tax IRA assets to Roth before your RMD age can reduce future required distributions. Conversions increase taxable income now but reduce it later.

- Qualified Charitable Distributions (QCDs): Retirees age 70½ or older can donate up to $111,000 per year (2026 limit, indexed for inflation) directly from an IRA to charity. A QCD satisfies your RMD without being included in your taxable income.

- Asset location decisions: When RMDs require liquidating assets, which holdings are sold — and in which account — becomes both a tax decision and an investment decision.

- Estimated tax and withholding: RMDs that are larger than expected can create underpayment penalties if estimated taxes or withholding are not adjusted accordingly.

Required minimum distributions are not simply a compliance task. For retirees with significant pre-tax assets, they are one of the most impactful variables in retirement income planning — and one of the most overlooked opportunities for proactive tax management.

Frequently Asked Questions About Required Minimum Distributions

Do I owe taxes on my RMD?

Yes. Withdrawals from traditional IRAs and employer-sponsored plans like 401(k)s are taxed as ordinary income in the year you take them. The IRS deferred taxes on these accounts when you contributed; RMDs are how that bill eventually comes due.

The amount you withdraw gets added to your other income for the year, which means a larger RMD can push you into a higher tax bracket, increase the portion of your Social Security benefits that’s taxed, or trigger Medicare IRMAA surcharges on your Part B and D premiums.

What happens if I miss a required minimum distribution?

If you fail to take your full RMD by the deadline, the IRS may impose an excise tax of 25% on the shortfall (reduced from 50% under SECURE 2.0). The penalty may be further reduced to 10% if the error is corrected within the correction window. You should also file IRS Form 5329 to report and calculate the penalty. A financial advisor can help you navigate corrective distributions.

Can I take more than my RMD?

Yes. You may always withdraw more than the required minimum amount. However, any excess withdrawal does not reduce future RMDs — each year’s distribution is calculated independently based on your December 31 account balance and life expectancy factor.

Can I donate my RMD to charity?

Yes. If you are age 70½ or older, you can make a Qualified Charitable Distribution (QCD) directly from your IRA to a qualified charity. A QCD counts toward your annual RMD and is excluded from your taxable income. For 2026, the annual QCD limit is $111,000 per person. This strategy is particularly effective for retirees who regularly donate to charity and want to manage taxable income.

Work With a CFP® on Your RMD Strategy

Required minimum distributions are not a once-a-year checkbox. They’re a moving target shaped by account type, balance, age, employment status, and tax law — and the more accounts you have, the greater the risk of an overlooked deadline or a costly miscalculation.

At HTG Advisors, our CERTIFIED FINANCIAL PLANNER® professionals take the complexity out of RMDs by inventorying every retirement account, coordinating distributions across custodians, and integrating your required minimum distributions into a broader tax and income planning strategy.

Whether you’re approaching your required beginning date, managing distributions across multiple accounts, or navigating the rules for an inherited IRA, we can help you stay on track — and make the most of every dollar.