Changing jobs is exciting — but it comes with one important financial question most people overlook: what happens to your 401(k)? CFP® certificant Allison Donaldson shares what you should consider before deciding which option is right for you.

The average American changes jobs over a dozen times before retiring1. That means most people will face this decision more than once. And yet, a large percentage of employees cash out their 401(k) when they leave a job — a move that can trigger thousands of dollars in taxes and penalties, and derail decades of retirement savings.

The good news? You have options. And making the right choice — even just once — can mean the difference between a comfortable retirement and scrambling to catch up.

This guide walks you through exactly what happens to your 401(k) when you leave a job, your four main choices, and how to decide which option is right for your situation.

Table of Contents

- The True Cost of Cashing Out Your 401(k) — And Why You Should Avoid It

- Option 1: Leave Your 401(k) With Your Former Employer

- Option 2: Roll Your 401(k) Into Your New Employer’s Plan

- Option 3: Roll Your 401(k) Into an IRA

- What If Your 401(k) Has a Roth Portion?

- Frequently Asked Questions

- Next Steps: Get Personalized 401(k) Guidance

The True Cost of Cashing Out Your 401(k)

Before we walk through your options, let’s address the most common — and most costly — mistake: cashing out.

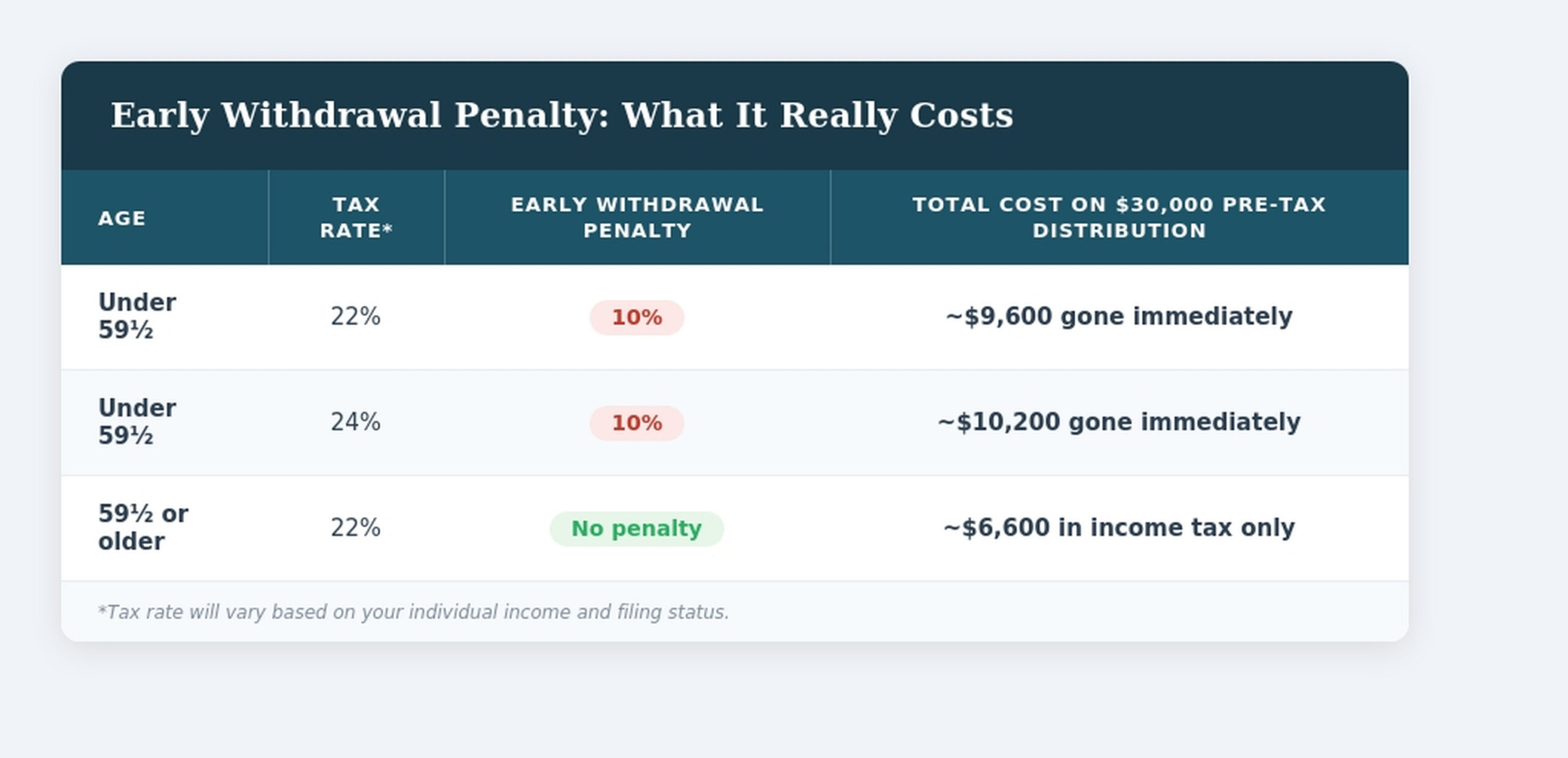

If you withdraw from your 401(k) before age 59½, you’ll face two immediate hits:

- A 10% early withdrawal penalty on the entire balance

- Ordinary income tax on the full pre-tax amount (federal + potentially state)

On a $30,000 balance, that can mean $9,000–$10,000+ owed in taxes and penalties — money that’s gone from your savings the moment you take the distribution.

But the immediate tax hit is only part of the story. Cashing out costs you in a third, less visible way: the permanent loss of years of tax-deferred growth. The money you withdraw doesn’t just disappear — it stops compounding. The impact 20–30 years from now is often multiples of what you took out today.

Lost tax-deferred growth

Consider Lauren, age 30, with $30,000 in her 401(k) when she changes jobs:

Cashing out is technically one of your four options — but it’s almost always the worst one. Unless you’re facing a genuine financial emergency with no other resources, the combination of immediate penalties, taxes, and lost compounding makes it extremely difficult to recover from.

Note: A limited number of hardship withdrawal exceptions may waive the 10% penalty — but income taxes still apply. Consult a financial advisor before taking this step.

Option 1: Leave Your 401(k) With Your Former Employer

In most cases, if your balance exceeds $5,000, your former employer must allow you to leave your 401(k) in their plan — at least temporarily. This is the path of least resistance, but it comes with trade-offs.

✅ Advantages

- Simplest option — no paperwork, no tax considerations, no transfers

- Potential preferential tax treatment on appreciated company stock (Net Unrealized Appreciation rules)

- Maintains existing investment allocations without disruption

- Strong creditor protection — ERISA-governed 401(k) plans offer robust federal protection from creditors and bankruptcy. IRA protections vary by state and are generally weaker

⚠️ Disadvantages

- Easy to “forget” this account and lose sight of it in your overall retirement savings

- As a former employee, your access to funds may be more restricted — ask about the plan’s rules

- You may be charged additional administrative fees as a non-active participant

- Harder to maintain a cohesive investment strategy across multiple old accounts

Best for: People who need a short-term holding period while they evaluate their options, or who have significant company stock with embedded gains.

Option 2: Roll Your 401(k) Into Your New Employer’s Plan

If your new employer offers a 401(k) plan, you may be able to roll your old balance directly into it. This is a smart choice for people who want to consolidate their retirement accounts and keep things simple.

✅ Advantages

- Tax and penalty-free transfer — no early withdrawal penalties if done correctly

- Consolidates retirement assets, making it easier to maintain a unified investment strategy

- New plan may offer better investment options, lower fees, or additional services

- Many 401(k) plans allow active employees to borrow against their balance in certain circumstances

⚠️ Disadvantages

- New plan may offer fewer investment options than an IRA

- May require a waiting period before you’re eligible to participate

- You’re subject to the new plan’s rules, which may be more restrictive

Best for: People who want simplicity and a single account, prefer access to a loan option, and are comfortable with the new plan’s investment lineup.

Option 3: Roll Your 401(k) Into an IRA

Rolling your 401(k) into an Individual Retirement Account (IRA) is often the most flexible option. An IRA gives you complete control over your investments and offers more planning options than most employer-sponsored plans.

✅ Advantages

- Tax-and penalty- free direct rollover — no taxes or penalties if handled correctly

- Dramatically broader investment choices: stocks, bonds, ETFs, mutual funds, REITs, and more

- Easier to consolidate multiple old 401(k)s into a single, cohesive investment strategy

- More flexibility in naming beneficiaries — in a 401(k), your spouse is the default beneficiary unless they formally waive that right; in an IRA, you can name anyone

- More exceptions to the 10% early withdrawal penalty are available with an IRA (e.g., first home purchase, qualified education expenses, disability)

⚠️ Disadvantages

- No loan option — unlike many 401(k) plans, IRAs cannot be borrowed against

- Fees vary widely — an IRA isn’t automatically cheaper; compare expense ratios and account fees before deciding

- May complicate backdoor Roth contributions — if you have significant pre-tax IRA assets, the pro-rata rule can make this strategy costly or impractical

- Eliminates access to the Rule of 55 — if you’re in your mid-to-late 50s and leave your job, funds in a former employer’s 401(k) may be accessible penalty-free; once rolled to an IRA, that option is gone

Best for: People who want maximum investment flexibility, are consolidating multiple accounts, or have complex estate planning or beneficiary needs.

What If Your 401(k) Has a Roth Portion?

More employers now offer a Roth 401(k) option alongside a traditional 401(k) — and many employees have been contributing to both without fully understanding that the two buckets follow different rules when you leave a job. If your account includes a Roth portion, here’s what you need to know.

How Roth 401(k) Contributions Are Different

Traditional 401(k) contributions are made pre-tax — you pay taxes when you withdraw in retirement. Roth 401(k) contributions are made after-tax, which means qualified withdrawals in retirement are completely tax-free, including the growth. That distinction matters a great deal when you decide what to do with your money at a job change.

Rolling Over Your Roth 401(k)

The same four options described above apply to your Roth balance — but the details differ. In practice, most plans distribute your traditional and Roth balances together, so you’ll typically be making one decision that covers both portions rather than choosing separately for each.

- Roll to a new employer’s Roth 401(k): If your new employer’s plan accepts incoming Roth rollovers (not all do — confirm first), this keeps your money in an employer plan and preserves the tax-free growth. Your after-tax contribution basis should transfer with the rollover, but confirm with the new plan how incoming rollover basis is tracked, as recordkeeping practices vary.

- Roll to a Roth IRA: This is often the most advantageous move. A Roth IRA has no required minimum distributions (RMDs) during your lifetime. Rolling into a Roth IRA also gives you the broader investment flexibility described in Option 3 above. Your contribution basis transfers with the rollover, preserving the tax-free nature of your original contributions.

- Leave it with your former employer: The same short-term holding considerations apply. The Roth portion remains separately tracked within the plan.

- Cash out: This is especially costly with a Roth 401(k). If you haven’t met the five-year holding rule or aren’t yet 59½, the earnings portion of your distribution will be taxable and subject to the 10% penalty — even though you already paid tax on your contributions. You lose the very tax advantage you were building toward.

The Five-Year Rule

For Roth 401(k) earnings to be distributed tax-free, the account must satisfy a five-year holding period. Importantly, if you roll your Roth 401(k) into a Roth IRA, the five-year clock for the IRA may differ from the one on your 401(k). If you already have an established Roth IRA, the IRA’s five-year clock governs — which could be in your favor. If you’re opening a new Roth IRA for the rollover, the five-year period starts fresh. This is a nuanced but meaningful distinction — talk to your financial advisor before rolling over.

Frequently Asked Questions About Your 401(k) and Job Changes

How long do I have to roll over my 401(k) after leaving a job?

If a distribution is made payable to you directly, you generally have 60 days from the date you receive a distribution to roll it over into another qualified plan or IRA without tax consequences. Missing this window triggers taxes and potential penalties. A direct rollover (trustee-to-trustee transfer) avoids this deadline entirely and is strongly preferred.

Can my former employer force me to take my 401(k) out?

If your balance is less than $1,000, your employer may automatically cash it out. For balances between $1,000 and $5,000, they may roll it into an IRA on your behalf. For balances over $5,000, they must allow you to keep it in the plan — at least until you reach retirement age.

What is a direct rollover vs. an indirect rollover?

A direct rollover sends funds directly from your old plan to your new plan or IRA — you never receive the money, so there are no taxes withheld. An indirect rollover sends the funds to you first; your employer withholds 20% for taxes, and you must deposit the full original amount (including that withheld 20%) into a new account within 60 days to avoid taxes and penalties.

What if I have company stock in my 401(k)?

If you hold your employer’s stock in your 401(k), Net Unrealized Appreciation (NUA) rules may allow for more favorable tax treatment. This is a nuanced area — consult with a financial planner before rolling over company stock.

How do I roll over my 401(k) into an IRA?

Contact your old plan administrator and request a direct rollover to an IRA custodian of your choice. Open an IRA if you don’t have one, provide the rollover instructions, and the funds will be transferred directly — typically within 1–2 weeks.

What is the Rule of 55, and how does it affect 401(k) withdrawals?

The Rule of 55 is an IRS provision that allows workers who separate from service and are at least age 55 to withdraw money from their employer-sponsored 401(k) or 403(b) plan without paying the usual 10% early withdrawal penalty — even if they’re under age 59½. Withdrawals are still treated as ordinary income and taxed accordingly.

While the Rule of 55 can be a helpful bridge for people who retire early or experience a job transition in their mid-to-late 50s, there are several important rules and restrictions that apply — including how taxes are treated, which accounts qualify, and timing requirements around when you leave your job. Contact your financial advisor to understand how this rule applies to your specific situation.

What happens to the Roth portion of my 401(k) when I leave a job?

Your Roth 401(k) balance follows the same general options as your traditional balance — you can leave it, roll it to a new employer plan, roll it to a Roth IRA, or (unwisely) cash it out. The key difference is the tax treatment: because you already paid income tax on Roth contributions, a properly executed rollover to a Roth IRA keeps all that future growth tax-free. Rolling to a Roth IRA is usually the best move, as it also eliminates required minimum distributions that previously applied to Roth 401(k) accounts. See the “What If Your 401(k) Has a Roth Portion?” section above for a full breakdown, and consult a financial advisor to understand how the five-year rule applies to your situation.

For a full overview of which accounts can be rolled into which, see the IRS Rollover Chart — What Can Be Rolled Over to What.

Next Steps: Get Personalized 401(k) Guidance

Changing jobs is one of the most common — and highest-stakes — financial decisions you’ll make. The right move for your 401(k) depends on your income, tax situation, timeline, investment goals, and the specific plans available to you.

At HTG Advisors, our CERTIFIED FINANCIAL PLANNER® professionals specialize in retirement planning, investment management, and tax-smart strategies for people navigating major life transitions. We’ll help you evaluate every option — and make a decision you’ll feel confident about for decades to come.