Should I front-load or max out my 401(k) early in the year? How do I avoid losing my company match?

These questions came up recently when my husband prepared for his annual bonus elections in January. After consulting with our CFP® colleagues at HTG, we discovered the answer isn’t one-size-fits-all—it requires careful analysis of your specific circumstances. This blog breaks down the benefits and drawbacks of 401(k) front-loading strategies and how a CERTIFIED FINANCIAL PLANNER® helps you optimize your retirement contributions.

Table of Contents

- What is 401(k) Front-Loading?

- The Most Important Factor: Your Company 401(k) Match and True-Up

- Front-Loading from Bonus vs. Regular Paychecks

- Benefits of Front-Loading Your 401(k)

- Drawbacks of Front-Loading Your 401(k)

- How to Decide What’s Right for You

- How a CERTIFIED FINANCIAL PLANNER® Can Help

What is 401(k) Front-Loading?

Front-loading your 401(k) means maxing out your annual contribution limit as early in the year as possible—often within the first few months—rather than spreading contributions evenly across all paychecks. This strategy has gained popularity among high earners and retirement-focused savers looking to maximize time in the market. But is front-loading the right strategy for you? The answer depends on several critical factors, including your company’s matching policy, your cash flow needs, and your overall financial situation.

The Most Important Factor: Your Company 401(k) Match and True-Up

Before you consider front-loading your 401(k), you need to understand exactly how your company’s matching contribution works. This single factor can make or break a front-loading strategy, potentially costing you thousands of dollars if you get it wrong.

Understanding Your Company Match Structure

Locate your Summary Plan Description (SPD) and answer these critical questions:

- What counts as eligible compensation (e.g., does your bonus count)?

- Is the match calculated per paycheck or annually?

- Does your company offer a “true-up” contribution?

What Is a 401(k) True-Up?

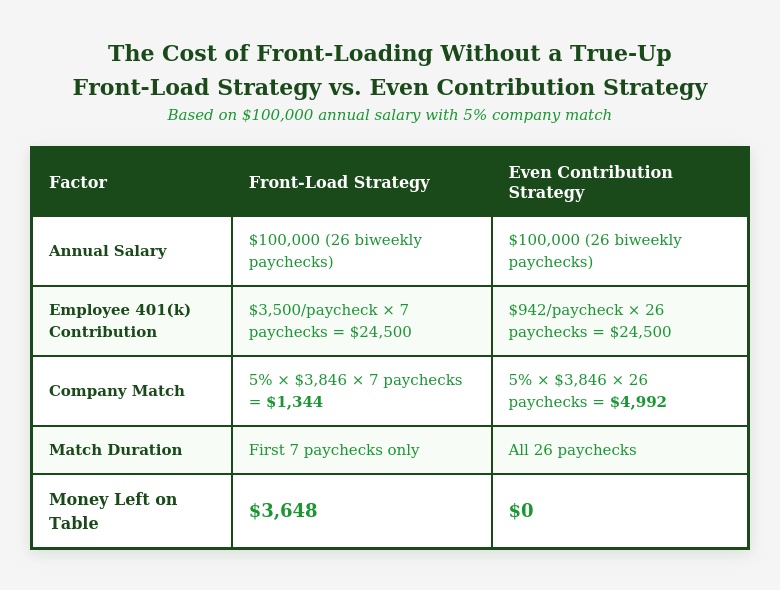

A true-up is a reconciliation payment your company makes (typically in the following year) to ensure you received your full match based on your total annual compensation, regardless of when you made your contributions throughout the year.

Why this matters: Many companies calculate their match on a per-paycheck basis. If you max out your 401(k) early and stop contributing, you might stop receiving matching dollars for the rest of the year—even though you’re still earning a salary.

Here’s a real-world scenario showing how much money you could lose without a 401(k) true-up plan:  If your company offers a true-up, they’ll reconcile at year-end and pay you the $3,648 difference. If they don’t offer a true-up, you lose that money permanently.

If your company offers a true-up, they’ll reconcile at year-end and pay you the $3,648 difference. If they don’t offer a true-up, you lose that money permanently.

Bottom line: Never front-load your 401(k) without first confirming your company’s match policy. A single conversation with HR can save you thousands of dollars.

Front-Loading from Bonus vs. Regular Paychecks

How you front-load matters just as much as whether you front-load. There are two main approaches, each with distinct advantages and considerations.

Front-Loading from an Annual Bonus

If you receive a substantial annual bonus, contributing a large portion to your 401(k) from that bonus can be an attractive option.

Advantages

- Preserves regular cash flow. Your regular paychecks remain unchanged throughout the year, maintaining consistent cash flow for everyday expenses.

- Allocates “extra” money. You’re using bonus income rather than reducing your base living standard.

- Less psychological impact. Since you may not have been counting on the full bonus amount, the contribution feels less restrictive.

- Allows continued smaller contributions. You can still make smaller contributions from regular paychecks for the rest of the year.

Considerations

- Verify eligible compensation. Make sure your bonus counts as “eligible compensation” for company match purposes (check your SPD).

- Calculate optimal split. Determine how much to contribute from the bonus versus spreading throughout the year to optimize both the match and your cash flow needs.

- Confirm processing mechanics. Some companies process bonus contributions differently, so verify the details with your payroll department.

Front-Loading from Regular Paychecks

This means making very large contributions from your regular salary early in the year until you hit the annual maximum (2026 limit is $24,500 for those under 50 and $31,000 for those 50+).

Advantages

- Immediate implementation. You can start immediately in January without waiting for a bonus.

- Universal applicability. Works for anyone, regardless of bonus structure.

Considerations

- Significantly reduced take-home pay. This dramatically reduces your paycheck during the front-loading period, which could strain your budget.

- Requires substantial emergency savings. You’ll need adequate reserves to cover expenses during the low-paycheck months.

- Creates cash flow volatility. Expect lower paychecks early in the year, then higher paychecks later.

- Demands careful planning. You must ensure you can cover fixed expenses like mortgage, insurance, and other non-negotiable costs.

Which Approach Makes More Sense?

Front-loading from a bonus is generally preferable if you have the option because it allows you to maximize time in the market without disrupting your regular cash flow. However, the best choice depends on your specific situation, including the size of your bonus, your expense timing, and your overall cash reserves.

Benefits of Front-Loading Your 401(k)

Once you’ve confirmed you won’t lose company match dollars and determined your front-loading method, here are the key advantages:

- Maximize Time in the Market

Investment markets have historically grown over time. Since 1957, the S&P 500 has generated average annual returns of over 10%.¹ Getting your money invested earlier gives it more time to potentially benefit from that growth. If you contribute $24,500 in January versus spreading it throughout the year, that early money has up to 11 additional months of market exposure compared to your final contributions. Research consistently shows that time in the market beats timing the market.

- Tax-Deferred Growth Starts Sooner

The earlier your contributions go in, the sooner they begin growing tax-deferred. While the difference may seem small year-to-year, compounding over decades can be meaningful. Strategic tax planning can help you maximize the benefits of tax-deferred growth.

- Higher Take-Home Pay Later in the Year

After maxing out early, your paychecks for the rest of the year will be larger since you’re no longer making 401(k) deductions. This provides flexibility for other financial goals or expenses that arise later in the year.

- Simplified Planning

You’ve checked the box on retirement savings early and can focus on other financial priorities for the rest of the year.

- Protection Against Mid-Year Job Changes

If you change employers mid-year or face job loss, front-loading ensures you’ve already maximized your 401(k) contribution for the year, avoiding potential gaps in your retirement savings.

Drawbacks of Front-Loading Your 401(k)

Front-loading isn’t the right choice for everyone. Here are the potential downsides:

- Reduced Cash Flow Early in the Year

Making large 401(k) contributions means smaller paychecks early in the year when you might need cash for annual expenses like property taxes, insurance premiums, or holiday spending carryover. Important: Don’t front-load unless you have a strong emergency fund. Even with adequate reserves, you should intentionally plan to rebuild your emergency fund toward the end of the year.

- No Dollar-Cost Averaging

When you spread contributions throughout the year, you naturally buy at different price points—sometimes when the market is high, sometimes when it’s low. This is called dollar-cost averaging, and it can reduce the impact of market volatility. Front-loading means you’re making one big bet on market timing, even if that’s not your intention. If the market drops significantly after you invest, you’ve purchased at relatively high prices.

- Delayed Company Match (If Relying on True-Up)

If your company pays the true-up in the following year, those matching dollars arrive months later than they would with even contributions. This means:

- Less time in the market for those specific dollars

- Potential risk if you leave the company before the true-up is paid

- Less Flexibility to Adjust

Once you’ve front-loaded, you can’t easily reduce or pause contributions if your financial situation changes mid-year. With even contributions, you have more flexibility to adjust as needed.

- Cash Flow Management Challenges

Requires substantial emergency savings and careful budgeting to cover living expenses during months with reduced paychecks.

How to Decide What’s Right for You

After weighing all the factors, here are clear guidelines for choosing your 401(k) contribution strategy: Consider Front-Loading from a Bonus If:

- You receive a substantial annual bonus

- Your bonus counts as eligible compensation for the company match

- You want to invest early without disrupting regular cash flow

- Your company offers a true-up (or calculates match annually)

- You have sufficient emergency savings

Consider Front-Loading from Regular Paychecks If:

- You don’t receive a bonus (or it’s not substantial enough)

- You have significant cash reserves to cover reduced paychecks

- Your fixed expenses are low relative to your salary

- Your company offers a true-up

- You’re comfortable with dramatic cash flow swings

Consider Spreading Contributions Evenly If:

- Your company doesn’t offer a true-up

- You prefer dollar-cost averaging

- You need consistent cash flow throughout the year

- You value flexibility to adjust contributions mid-year

- You’re risk-averse about market timing

- You don’t have substantial cash reserves

Consider a Hybrid Approach If:

- You want some benefits of both strategies

- You receive a bonus but want to hedge your bets

- You prefer not to overthink the decision

- You want to mitigate market timing risk

Our Real-World Hybrid Solution After analyzing the pros and cons, my husband and I landed on a 50/50 strategy that takes advantage of his annual bonus:

- Contribute roughly half of the annual limit from his January bonus

- Spread the remaining contributions evenly throughout the year from regular paychecks

This approach gives us meaningful early market exposure without going all-in on timing, some dollar-cost averaging benefits through the year, consistent cash flow, no budget strain, and peace of mind that we’re not overthinking it.

How a CERTIFIED FINANCIAL PLANNER® Can Help

At HTG Advisors, our CERTIFIED FINANCIAL PLANNERS® help clients optimize 401(k) contribution strategies as part of comprehensive retirement planning. We evaluate:

- Your complete financial picture. We consider how your 401(k) strategy integrates with your emergency fund, tax situation, other retirement accounts, and long-term goals.

- Company match analysis. We review your Summary Plan Description to determine the optimal contribution timing that maximizes your employer match.

- Cash flow modeling. We project the impact of different contribution strategies on your monthly cash flow to ensure you can comfortably maintain your lifestyle.

- Tax optimization. We coordinate your 401(k) contributions with other tax planning strategies to minimize your lifetime tax burden.

- Ongoing adjustments. As your income, company policies, or market conditions change, we help you adapt your strategy.

Learn more about our comprehensive approach to investment management and retirement planning. Remember, the most important thing is that you’re contributing to your 401(k) at all. Whether you front-load, spread evenly, or take a hybrid approach, you’re making a smart move for your financial future. Ready to optimize your 401(k) strategy? Contact HTG Advisors today to work with a CERTIFIED FINANCIAL PLANNER® who can analyze your company’s match structure, evaluate your cash flow needs, and develop a contribution strategy aligned with your retirement goals.

BOOK A FREE CONSULTATION TODAY

¹Fidelity. “What is the S&P 500 and stock market average return?” Fidelity Investments. Updated 2025.