This guide walks you through exactly what causes impulse buying, the real financial damage it causes, and nine practical strategies to stop.

Maybe you stopped at the supermarket on the way home, hungry, and grabbed everything in sight. Maybe you were scrolling social media and the sale was too good to scroll past. Or maybe you just needed to do something after a rough day at work — and retail therapy felt like a reward you deserved. Whatever the trigger, the result is the same: bags of stuff you didn’t need, and a quiet question afterward — why did I do that?

The good news? Impulse buying is driven by predictable triggers — which means it can be managed. Once you understand what’s pulling you toward the checkout button, you can take back control.

Table of Contents

- What Is Impulse Buying?

- The Real Financial Cost of Impulse Shopping

- What Makes Us Impulse Shop?

- The 4 Types of Impulse Purchases

- How Impulse Buying Affects More Than Your Wallet

- Strategies to Stop Impulse Buying

- Impulse Buying at a Glance: Know Your Triggers

- Frequently Asked Questions About Impulse Buying

- Next Steps: Talk to a Financial Advisor

What Is Impulse Buying?

Impulse buying is any unplanned, spontaneous purchase made in the moment — without prior research, deliberation, or intention to buy. It happens in grocery stores, on social media, during late-night scrolling sessions, and after emotionally charged days.

It’s not a character flaw. It’s a response to how our brains, our environments, and modern marketing have all been designed to work together.

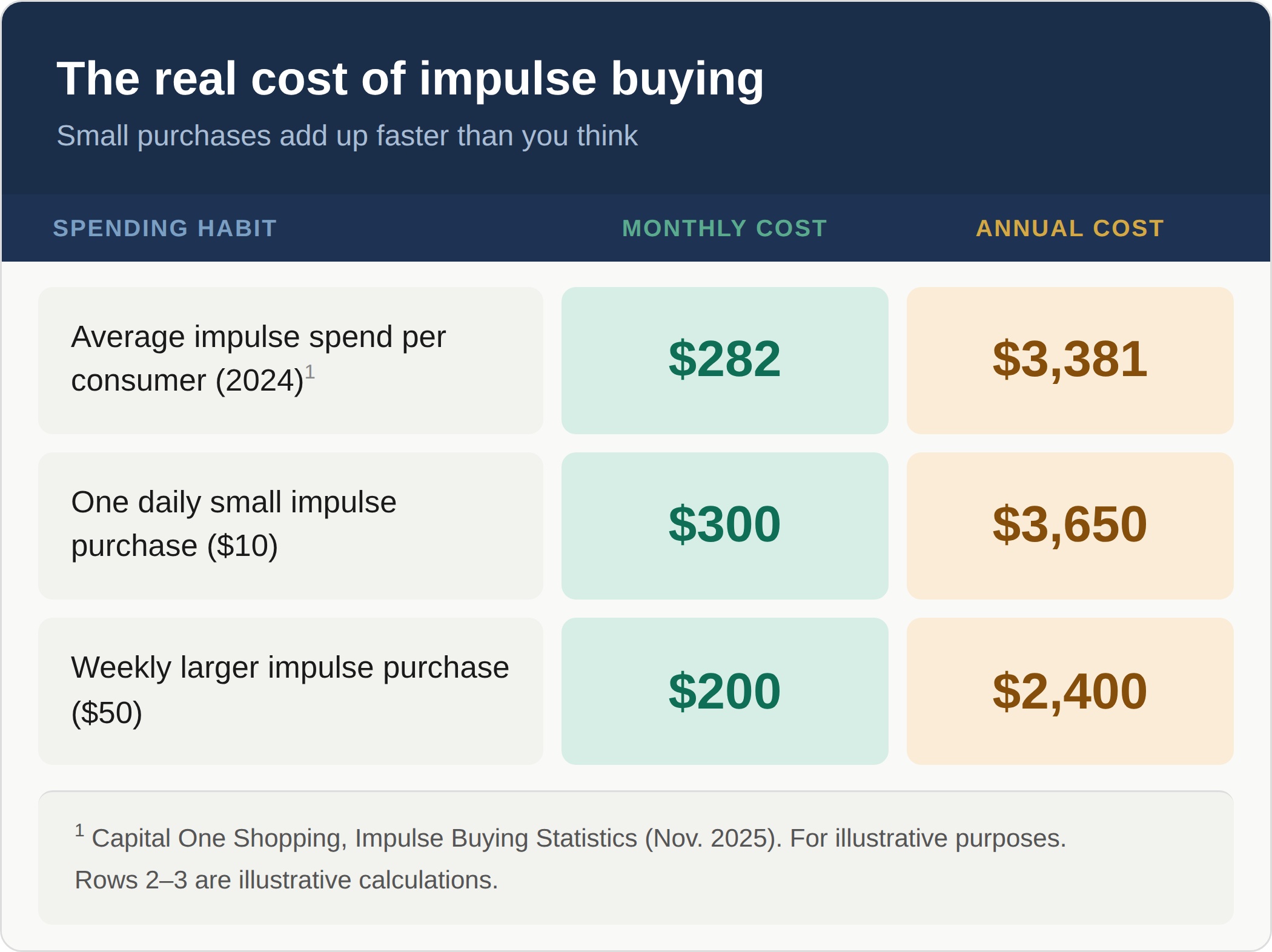

The Real Financial Cost of Impulse Shopping

Most people underestimate what impulse buying actually costs them. A $15 purchase here, a $40 splurge there — it feels harmless in the moment. But the numbers tell a different story. In 2024, the average consumer spent more than $280 per month on impulse purchases1 — adding up to nearly $3,400 a year in unplanned spending. At the same time, studies show that more than 70% of online shoppers have made an impulse purchase driven by discounts or promotions1, highlighting how common — and normalized — this behavior has become.

Beyond the immediate dollar amounts, chronic impulse spending can:

- Strain your monthly budget, leaving less room for savings, debt payoff, or planned purchases

- Increase your debt load, particularly if purchases go on — and if the balance isn’t paid off in full each month, the interest charges mean the true cost of that impulse buy keeps growing long after the purchase.

- Lower your credit score if increased balances affect your utilization ratio

- Undermine long-term financial goals like emergency funds, home ownership, or retirement

💡 Pro Tip: Track your unplanned purchases for just 30 days. Most people are genuinely surprised by the total — and that surprise alone is often enough to change behavior.

What Makes Us Impulse Shop?

Impulse buying isn’t random. It’s triggered by a predictable combination of psychological, emotional, and environmental factors.

Emotional State Boredom, stress, sadness, and anxiety all increase vulnerability to impulse purchases. The brain’s reward system activates and releases dopamine, creating a feeling of instant gratification — a brief emotional lift that can make a purchase feel justified in the moment.

Urgency-Based Marketing Online retailers are skilled at creating pressure to buy now. Limited-time offers, countdown timers, “only 3 left in stock” warnings, and flash sales all activate FOMO (fear of missing out) and compress the time available for thoughtful decision-making.

This strategy is especially effective in today’s digital economy. Global e-commerce sales surpassed $6 trillion in 20252, creating an environment where consumers are constantly exposed to purchasing opportunities — often designed to encourage fast, emotional decisions rather than careful ones.

Social Media and Influencers Platforms are built for browsing — which easily becomes buying. Influencer promotions, sponsored posts, and one-tap purchasing make the distance between “I saw it” and “I bought it” smaller than ever. Mobile shopping in particular reduces the friction that might otherwise slow a purchase down.

Physical Store Design Brick-and-mortar stores use layout, lighting, music, and product placement intentionally. Small, inexpensive items near the checkout exist for exactly one reason: they’re hard to resist in the moment. Shoppers are being influenced in ways they often don’t consciously notice.

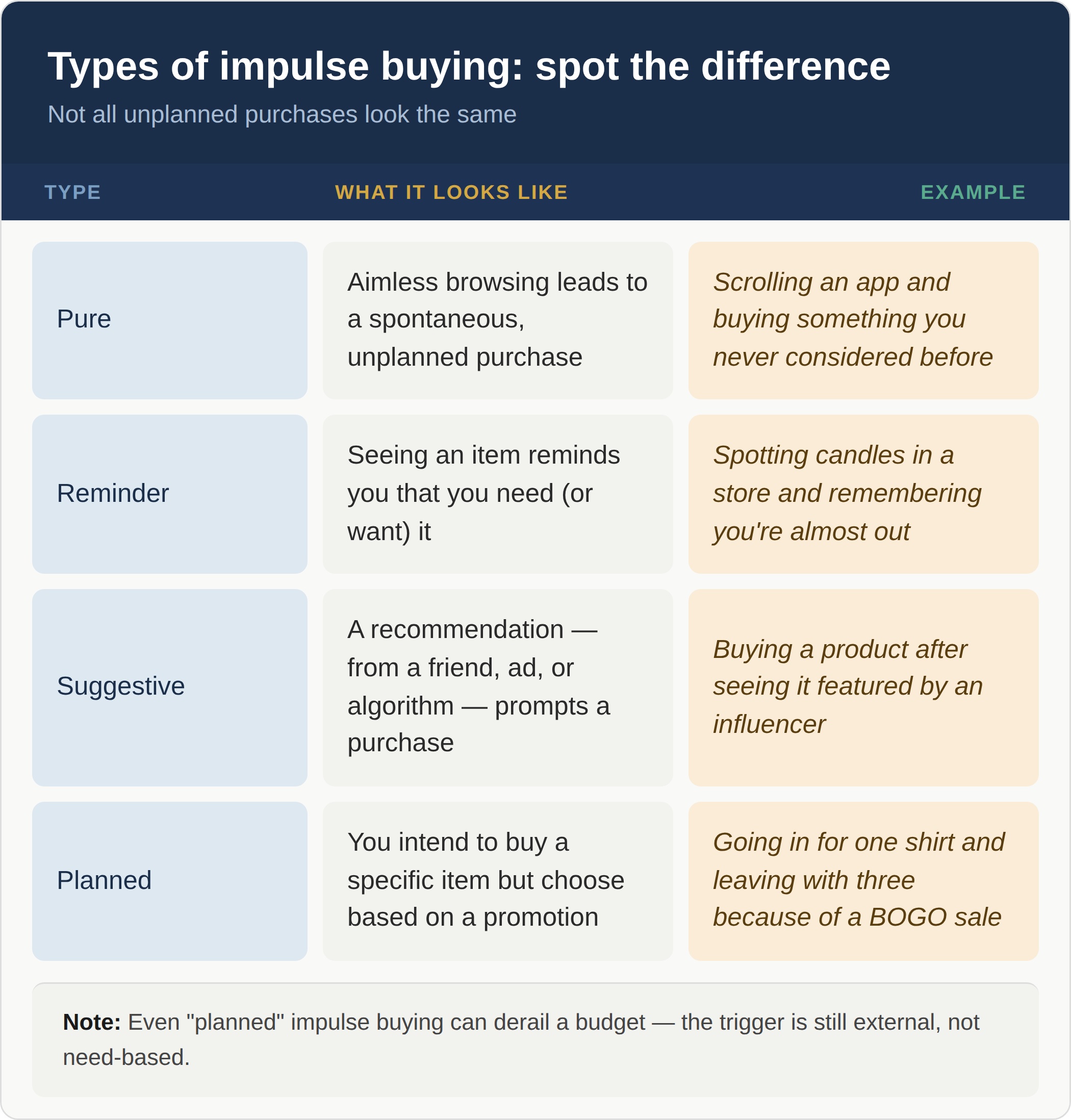

The 4 Types of Impulse Purchases

Researchers have identified four distinct types of impulse purchases. Recognizing which type you’re most prone to can help you intervene before you check out.

How Impulse Buying Affects More Than Your Wallet

The consequences of chronic impulse shopping extend beyond your bank account.

Decision-Making Fatigue Repeatedly giving into impulses weakens your overall self-control and discipline — not just in shopping, but in other areas of life. Every “yes” to an unplanned purchase makes the next one a little easier.

Stress and Regret The quick thrill of a purchase is often followed by buyer’s remorse — feelings of guilt, regret, and anxiety. Ironically, stress is one of the primary triggers for impulse shopping in the first place, creating a difficult cycle.

Cluttered Spaces Unplanned purchases accumulate. Over time, a home filled with things you don’t need or use creates its own form of stress and cognitive load.

Strategies to Stop Impulse Buying

You don’t have to eliminate shopping — you just need a plan that puts you back in the driver’s seat.

- Institute a cooling-off period. Wait 24–48 hours before completing any unplanned purchase. Revisit the item after the initial urge passes and ask yourself: do I still want or need this?

- Shop with a list. Whether it’s groceries or a shopping site, go in with a specific list and commit to buying only what’s on it. A list removes the “browsing” mode that leads to impulse purchases.

- Delete the apps. Remove shopping apps from your phone or computer. The harder it is to access a store, the less likely you are to impulse buy from it.

- Unsubscribe from promotional emails. Sale notifications and discount codes exist to pull you in. If the temptation never arrives in your inbox, it can’t trigger a purchase.

- Avoid shopping as entertainment. Browsing without intent to buy is one of the most common setups for impulse purchases. Find other ways to fill downtime.

- Track your spending. Review your bank or credit card statements with fresh eyes. Seeing exactly how much unplanned spending adds up is a powerful motivator.

- Remove saved payment methods. Friction is your friend. Requiring yourself to manually enter payment details adds a pause that can prevent automatic checkout behavior.

- Use a purchase checklist. Before completing any unplanned purchase, ask:

- Do I truly need this?

- How often will I realistically use or wear it?

- Will it hold its value?

- Does it fit into my financial goals?

- Recognize your emotional state. Impulse shopping spikes when you’re bored, stressed, or sad. If you notice you’re shopping to manage a feeling, that’s the signal to step away — and address the underlying emotion instead.

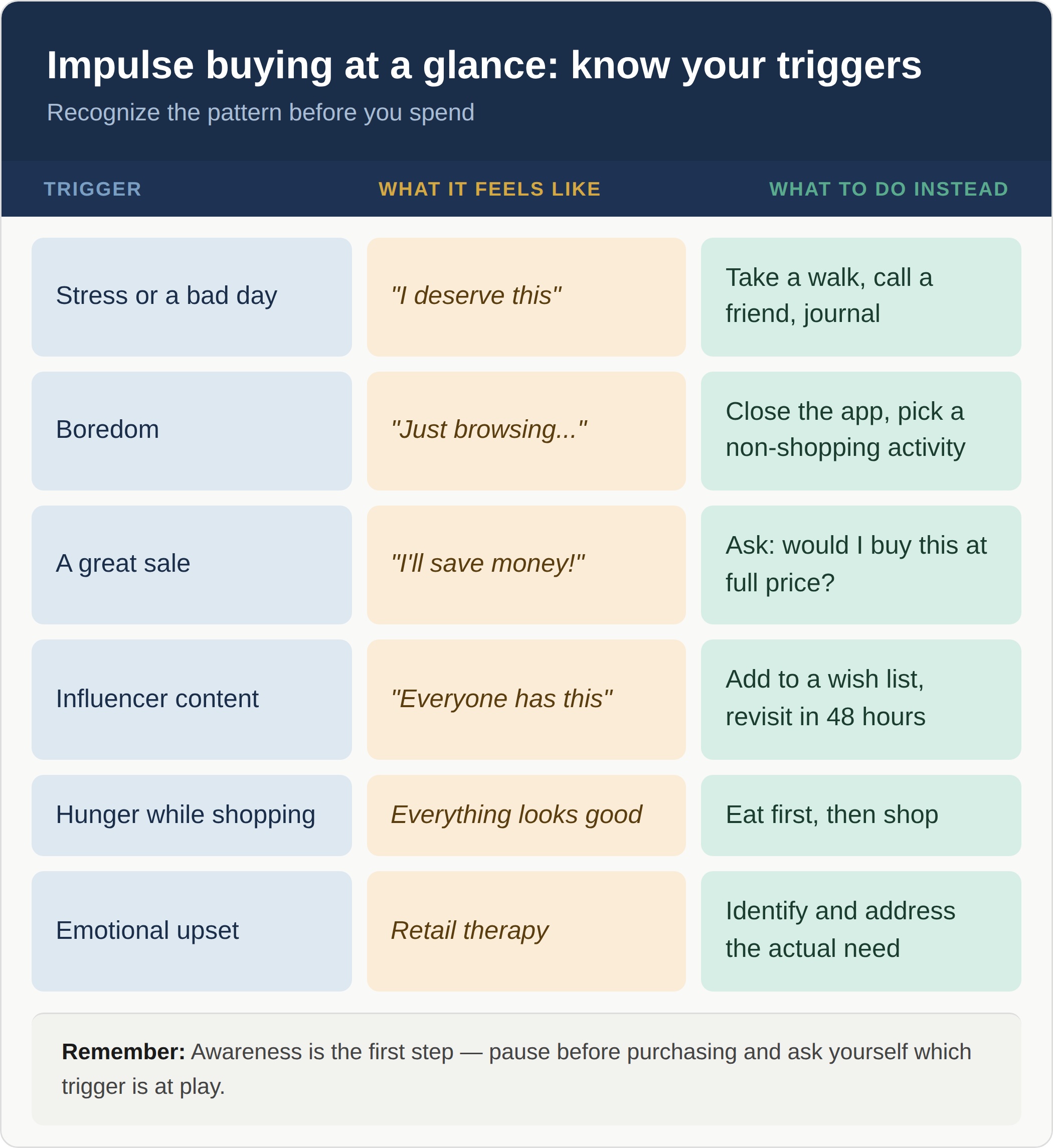

Impulse Buying at a Glance: Know Your Triggers

Frequently Asked Questions About Impulse Buying

Is impulse buying always a problem? Not necessarily. A small, affordable impulse purchase isn’t inherently harmful. The concern is when impulse buying becomes habitual, disrupts your budget, or is driven by emotional avoidance rather than genuine want or need.

Why do I feel good when I buy something, but bad afterward? The purchase triggers a dopamine release — a real neurological reward signal. But once the novelty fades, the cost (financial or emotional) becomes more salient. This gap between anticipation and satisfaction is well-documented in behavioral economics research.

Does the type of shopping matter — online vs. in-store? Yes. Research suggests mobile and online shopping lowers the psychological barriers to buying. The ease of one-click purchasing, combined with scrolling behavior, makes online environments particularly prone to impulse buying.

How do I know if my impulse buying is a serious problem? Signs that impulse buying has become a serious concern include: hiding purchases from a partner or family member, carrying ongoing credit card debt from unplanned purchases, feeling significant guilt or anxiety after buying, or an inability to stop despite wanting to.

Can a financial advisor help with impulse spending? Yes. A financial advisor can help you create a realistic budget that includes a discretionary “fun money” category — giving you “permission” to spend on things you enjoy, while protecting your broader financial goals.

Next Steps: Talk to a Financial Advisor

Impulse buying is one of the most common — and most quietly costly — financial habits we encounter. The good news is that it’s also one of the most manageable with the right awareness and structure.

At HTG Advisors, our CERTIFIED FINANCIAL PLANNER® professionals help clients build spending plans that reflect both their goals and their real lives. We’ll help you understand where your money is going, create a budget you can stick to, and make financial decisions you’ll feel good about — long after the purchase.

BOOK A FREE CONSULTATION TODAY

1 https://capitaloneshopping.com/research/impulse-buying-statistics/

2 https://www.shopify.com/blog/global-ecommerce-sales