Why do so many of us disregard the professional advice we are given? We know what is good for our health – exercise, eat right, get enough sleep, go to the doctor—but face barriers to doing them. The same goes for decisions that can improve our financial health.

Financial goals and tasks can be intimidating, which can cause people to avoid dealing with them. Good financial health isn’t easy and requires an honest look at your habits, biases, expectations, and cash flow. Just like going to the doctor and getting on the scale, this can be uncomfortable. But understanding these things is critical before you can improve your financial position. Since so many of us are stricken by procrastination and avoidance, I wondered: are there little tricks we can undertake to help us achieve better financial health?

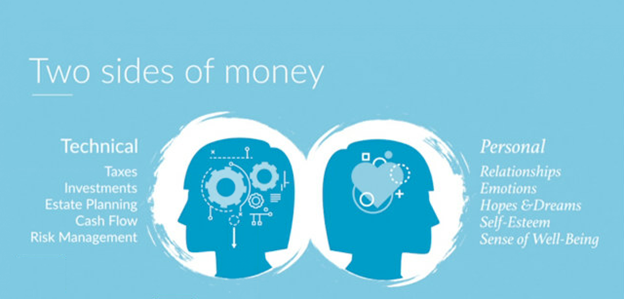

I recently listened to a webinar by Dr. Moira Somers, C. Psych, a family wealth psychologist with Money, Mind & Meaning. She framed our money decisions into technical (knowing what to do) and personal (how you feel about doing it) components. She then made the point that to satisfy the technical, we have to first appease the personal side of our decision-making. You may know what you need to do, but may dread, feel hopeless, intimidated, or lazy about doing it!

Source: Financial Transitionist Institute

“For better or for worse, the personal side [of our mind] has the ultimate decision-making power. That’s where the veto lies.”

Dr. Moira Somers

When faced with decisions, especially regarding our long-term wellness, it is human nature to default to our personal/emotional mind and choose the path of least resistance.

For example, I know I need to exercise more to improve my long-term health. With great intention, I go to bed early and set my alarm to give ample time for a morning workout. Yet in the morning, I feel tired, snooze my alarm (or perhaps turn it off altogether) and opt for an hour more of sleep instead of working out before work. My personal/emotional mind wins, and I opt for immediate gratification rather than choosing what I know is best for my long-term health.

And the farther off your goal, the harder it is to make good decisions towards that goal. Take, for example, a young adult in a first job who is just making ends meet. His employer offers a match on 401k contributions, but he is loath to give up even a little of his take-home pay. He will have to sacrifice an immediate want, like eating out during the week, to make progress towards his long-term goal of a comfortable retirement.

How can we overcome the inclination to choose the path of least resistance? There are ways to trick our personal/emotional mind into getting financial things done.

Here are five tips to get you started!

Schedule a regular time to address financial tasks

Whether weekly, monthly, or quarterly, schedule time on your calendar to focus on financial tasks. Creating a habit of addressing financial projects regularly can make them feel less overwhelming and keep you on track.

Break it up and choose a starting point

Many of your financial goals and priorities may feel overwhelming and out of reach. There are many different ways to accomplish a goal, but where can you begin? Break up the goal into actionable items and identify one or two steps you can take now towards that long-term goal.

Let’s take the need to save for retirement, for example, and break it down into easy action items. Your steps may look like this:

⇒ Save in a Roth IRA

- Compare and choose a custodian

- Open a new Roth account online

- Designate beneficiaries

- Set up monthly auto-deposit to save annual maximum

- Choose investments

⇒ Enroll in an employer retirement plan

- Contribute enough to 401k to take full advantage of the employer match

- Review investment options

Prioritize

Then, prioritize those steps.

Every pay period that goes by without enrolling in your 401k is money lost by forgoing the match. So, on your next scheduled financial focus day, log in to your benefits portal and choose to contribute that percentage of your income which takes full advantage of your employer match. Then choose as your first investment option a retirement-date fund that aligns with your expected retirement timeframe.

You’ve tackled your first task in three relatively easy steps that might take 15 minutes.

Keep things simple

Remember, you do not have to make complex choices for them to be good choices. Auto deposit, target date funds, and contributing enough to get your full company match will all simplify decisions.

To expand on the 401k example, don’t feel you need to research hundreds of securities or funds before making your investment choice when most plans offer a retirement-date or target-date fund that will suffice. (Be sure to evaluate the costs of your different options.)

Find a partner

Let’s admit it, sometimes we need support. Find a family member, friend, or financial advisor to be your cheerleader and keep you accountable.

Pat Yourself on the Back

Celebrate your small accomplishments and recognize their impact on the big picture.

These tips are a great place to start to move past emotional barriers and get you on your way to better financial wellness.