In times of market uncertainty, headlines about market drops and economic concerns can feel overwhelming, especially early in your investment journey. While experiencing volatility firsthand can test even the most resolute investor’s confidence, these fluctuations are both normal and manageable with the right approach.

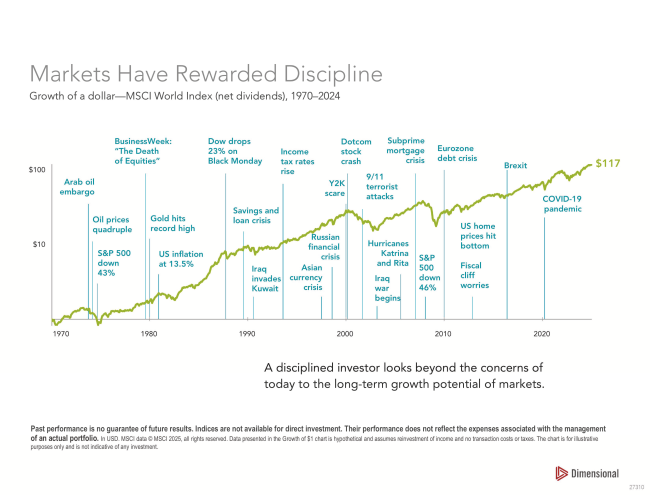

As the chart from Dimensional Fund Advisors below illustrates, market turbulence has been a recurring feature of financial landscapes throughout history—from the oil embargos of the 1970s to the recent COVID-19 pandemic.

click on chart to enlarge

Notice how each major market decline highlighted in the chart was ultimately followed by recovery and continued growth. This historical perspective serves as an important reminder that maintaining discipline during periods of volatility is an effective strategy for long-term investors.

Yet, how does one prepare to weather these periods of economic volatility? There are practical steps you can take to help you ‘ride out the storm’:

Build Your Financial Foundation First.

Before focusing exclusively on market investments, ensure you have a solid cash reserve. We recommend an emergency fund equal to 3-6 months of essential expenses in high-yield savings accounts, CD, or money market fund.

Match Your Investment Allocation with Your Time Horizon.

One of the most powerful strategies for managing volatility is properly aligning your investments with when you’ll need the money:

- Short-term goals (0-3 years): Primarily cash and short-term bonds

- Mid-term goals (3-7 years): Balanced mix of stocks, bonds, and cash

- Long-term goals (7+ years): Primarily growth-oriented investments

Remember that money you don’t need for 10+ years can withstand significant market fluctuations, giving you time to recover from downturns.

Diversification Is Your Shield.

A properly diversified portfolio remains your best protection against volatility:

- Spread investments across multiple asset classes (stocks, bonds, cash) according to your time horizon.

- Diversify within asset classes (different sectors, company sizes, geographic regions).

- Consider adding small allocations to alternative investments (like real estate) for additional diversification.

This approach ensures that when one area of your portfolio struggles, others may help offset those losses.

Don’t Let Emotions Derail Your Strategy.

Market volatility often triggers strong emotional responses that can lead to poor investment decisions:

- Avoid panic selling during downturns – historically, markets have recovered.

- Resist the urge to time the market – consistent investing typically outperforms.

- Stick to your plan – make portfolio adjustments based on life changes, not market movements.

- Consider automating your investment contributions to remove emotion from the equation.

With recent market fluctuations causing concern for many investors, it’s important to remember that building wealth is a long-term journey, and having the right strategies in place can help you navigate volatility with confidence.

Take Action:

- Calculate and build your emergency fund. Determine exactly how much you need and set up automatic transfers to a high-yield savings account until you reach your target.

- Document and categorize your goals by timeframe: 0-3 years, 3-7 years and 7+ years. Are they aligned accordingly with your investments? (more conservative for short-term, more growth-oriented for long-term).

- Automate your investment strategy: Set up recurring contributions on paydays, create a calendar for quarterly reviews only, and document specific rebalancing thresholds to remove emotion from investment decisions.