Most people assume their financial advisor is required to put their interests first. The type of advisor you work with, and the standard they follow, shapes how advice is given, how your advisor is compensated, and whether recommendations are built around you.

If you’ve ever wondered whether your advisor is legally required to act in your best interest, you’re asking exactly the right question, and the answer isn’t always yes.

CFP® Robin Sherwood has prepared a guide of what every investor should know about the key differences between a fiduciary advisor and a broker.

Table of Contents

- What Is a Fiduciary Financial Advisor?

- How Is the Fiduciary Standard Enforced?

- Are All Financial Advisors Fiduciaries?

- Fiduciary Advisor vs. Broker: Two Forms of Advice

- Frequently Asked Questions

- HTG Is a Fiduciary

1. What Is a Fiduciary Financial Advisor?

A fiduciary financial advisor is legally and ethically obligated to act in your best interest. That means providing advice and recommendations that are optimal for your specific situation, not just technically acceptable, and disclosing any conflicts of interest that could influence their guidance.

In practice, a fiduciary financial advisor will:

✅ Learn your goals, risk tolerance, and financial picture before recommending anything

✅ Recommend investments based on your needs, not on commission potential

✅ Disclose any compensation arrangements that could influence their guidance

✅ Provide transparent reporting on fees paid to them

✅ Accept payment only from you, not from third parties such as mutual fund companies, annuity providers, or firms whose investment products they may recommend

That last point matters. Many fiduciary advisors are fee-only, meaning the only money they earn comes directly from clients. There is no sales-related compensation, and there are no incentives to steer you toward one product or solution over another.

2. How Is the Fiduciary Standard Enforced?

The fiduciary duty isn’t just a philosophy advisors choose to follow. It’s tied to specific credentials and regulatory bodies that hold advisors accountable:

✅ CERTIFIED FINANCIAL PLANNER® professionals are required to act as fiduciaries by definition. The CFP® Board enforces this standard through a peer-review disciplinary process, with sanctions ranging from censure up to suspension or revocation of certification.

✅ NAPFA members must commit to a defined Fiduciary Standard, covering duties of care, loyalty, competence, compensation, and engagement, as a condition of membership.

✅ Investment Adviser Representatives (IARs) are held to a fiduciary standard under the Investment Advisers Act of 1940, with oversight from the SEC (or state securities regulators, depending on firm size).

In other words, this isn’t a marketing claim; it’s a designation and registration with real enforcement behind it. When choosing an advisor, asking which of these credentials and registrations they hold is one of the clearest ways to confirm they’re actually held to a fiduciary standard.

3. Are All Financial Advisors Fiduciaries?

No, and this is often a source of confusion for investors. The title “financial advisor” is a generic term that anyone can legally use. What is actually regulated is the specific legal standard of care the professional must follow.

Historically, the industry has operated under two entirely different rules: the rigid Fiduciary Standard (acting in your best interest, always) and the looser Suitability Standard (recommending products that fit your general profile). While modern regulations like the SEC’s 2020 Regulation Best Interest (Reg BI) have forced traditional brokers to raise their standards, they still do not fully replace a true, ongoing fiduciary obligation. Per Reg BI, brokers are now required to recommend what they genuinely believe is in your best interest at the time they make a recommendation, not just something that’s “good enough.” They’re also required to be more upfront about any conflicts of interest, such as earning higher compensation for recommending certain products.

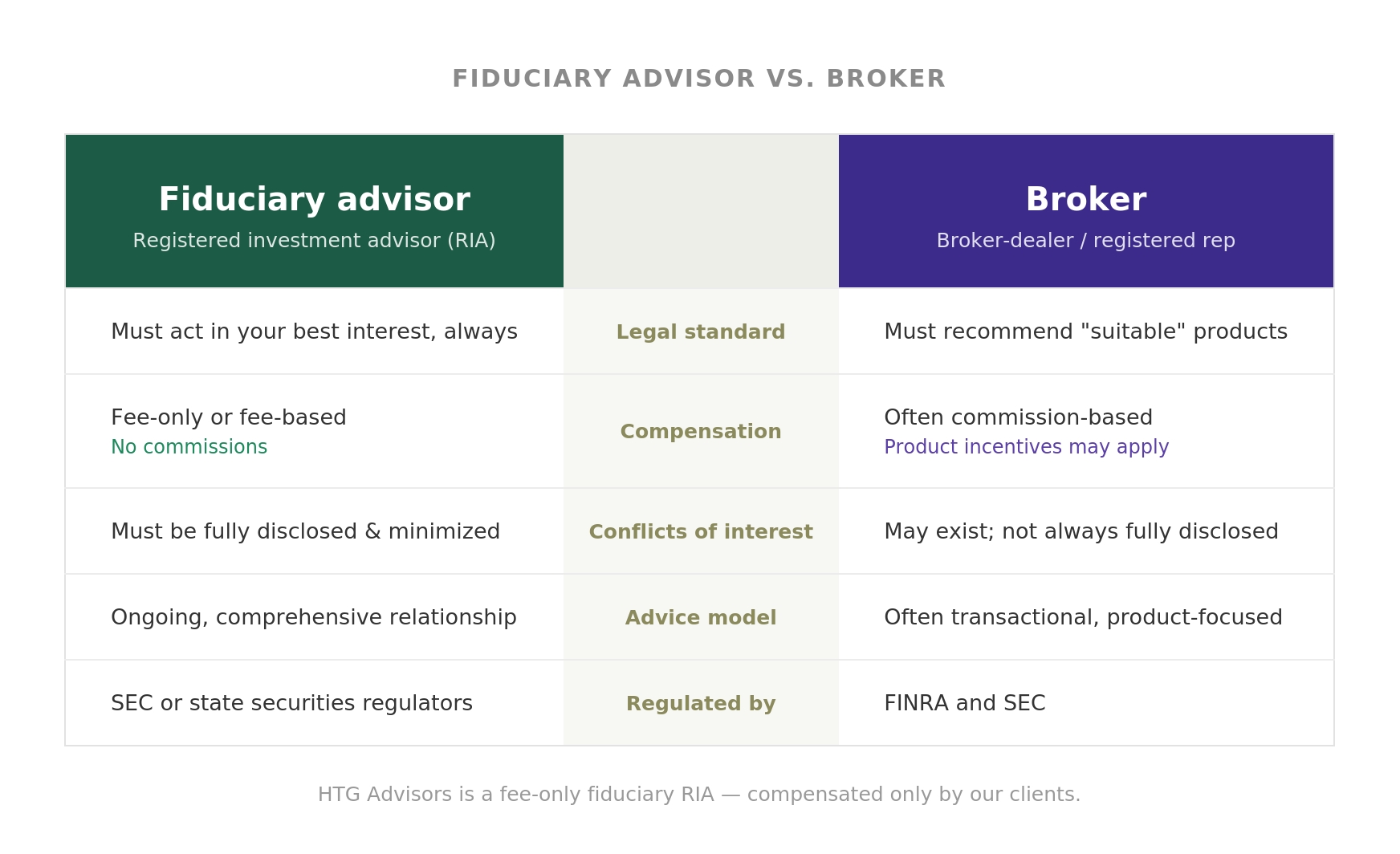

4. Fiduciary Advisor vs. Broker: Two Forms of Advice

As a result of these split regulations, two professionals who both call themselves “financial advisors” might be operating under completely different frameworks:

- Fiduciary Advisors: Professionals who provide ongoing advice tailored to your goals and are paid via transparent fees. This category prominently includes Certified Financial Planner (CFP®) professionals, who are strictly bound by the CFP Board’s fiduciary duty to act in their clients’ best interests at all times when providing financial advice.

- Brokers: Intermediaries who facilitate transactions and are typically compensated through commissions on the products they sell.

The breakdown below highlights exactly how these two approaches compare across five core dimensions:

5. Frequently Asked Questions

Can an advisor be both a broker and a fiduciary?

Yes. Some professionals hold both licenses, allowing them to act as a fiduciary in some situations and under the suitability standard in others. These “dual-registered,” or hybrid, advisors can create confusion for investors because the standard of care may shift depending on which hat they’re wearing. It’s worth asking any advisor directly which standard applies to your specific relationship.

How do I know if my current advisor is a fiduciary?

The most direct approach is simply to ask. You can also verify any investment advisor’s registration, licensing, and disciplinary history by looking up their firm name or CRD number on the SEC’s Investment Adviser Public Disclosure (IAPD) database.

Is fee-only the same as fiduciary?

Not exactly, but they often go together. “Fee-only” describes how the advisor earns compensation: exclusively from client fees, with zero commissions or product revenue. “Fiduciary” is the actual legal standard requiring the advisor to act in your best interest. Most fee-only advisors operate as fiduciaries, as a fee-only structure naturally eliminates the primary product-driven conflicts of interest that the fiduciary standard requires to be minimized.

Does working with a fiduciary guarantee better investment returns?

No. A fiduciary standard governs how advice is given and whose interests are being served, not the performance of the markets or individual investments. What it does provide is confidence that the advice you receive is designed around your goals, not around generating revenue for your advisor.

6. HTG Is a Fiduciary

When HTG Investment Advisors was founded more than three decades ago, we chose to operate as a fiduciary because we believed it was simply the right way to manage someone else’s wealth.

That commitment is still at the core of everything we do. As a fee-only Registered Investment Advisor, HTG will:

✅ Learn about you and your goals

✅ Provide transparency regarding fees, portfolio design, and reporting

✅ Manage discretionary portfolios based on your needs/goals

✅ Use independent, unaffiliated custodians

✅ Accept revenues solely from you, not commissions related to the buying and selling of products. We are a fee-only advisory firm.

With or without the regulation, HTG will always operate as a fiduciary. It’s woven into our original fabric.

To learn more about HTG Investment Advisors, read Our Story. Our investment management approach is built entirely around you: your circumstances, your goals, and your definition of financial success.

If you’re not sure whether your current advisor is a fiduciary, or if you’re looking for guidance that’s built entirely around your best interest, we’d welcome the opportunity to connect.

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor.