The 401(k) has replaced the traditional pension plan and represents the most common vehicle for building a retirement nest egg.

Since the average US employee changes jobs 11 times before retiring, it is likely that he or she will have multiple 401(k)s and no cohesive investment strategy.

Worse yet, 49% of employees cash out of their 401(k)s, potentially derailing their retirement planning entirely.

WHY NOT CASH OUT?

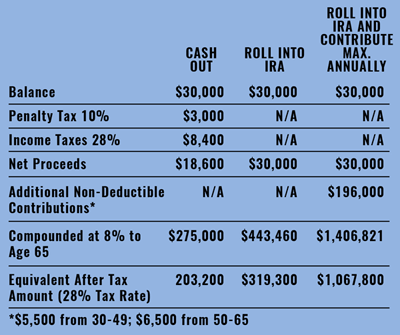

The penalties of cashing out are felt both at tax time and in the long-run when savings are insufficient to fund retirement. If you are under 59½, there is a 10% penalty for withdrawing from the 401(k) and the distribution is taxed as ordinary income. The overriding reason for not cashing out of a 401(k) is the loss of tax-deferred compounding. As seen below, starting retirement savings early, even with modest contributions, allows compounding to have a big impact.

Example: Lauren, Age 30 with $30,000 in 401(k) assets

The good news is that 401(k)s are portable. Once you have left your job, you have several options:

LEAVE IT AT YOUR FORMER EMPLOYER’S PLAN

Advantages

- Simplest option-no paperwork or worries about taxes and early withdrawal penalties.

- Preferential tax treatment of appreciated company stock upon withdrawal.

Disadvantages

- You may neglect these assets and not consider them in your retirement investment picture.

- As a former employee, access to your money may be more restricted. Ask about rules.

- Former employees may be charged extra fees.

ROLL IT OVER INTO YOUR NEW EMPLOYER’S PLAN

Advantages

- Tax-free transfer. No early withdrawal penalties.

- By consolidating retirement assets, you will more likely have a cohesive investment strategy.

- New plan may offer more attractive investment options or additional services.

- Most 401(k) plans allow employees to take a loan against the plan balance.

Disadvantages

- New plan may offer fewer investment options.

- New plan may require waiting period.

ROLL IT INTO AN IRA

Advantages

- Tax-free transfer.

- Broader investment choices in an IRA.

- Cohesive investment strategy and complete control by consolidating multiple plans.

- Flexibility in naming beneficiaries. In a 401(k), your spouse is named beneficiary, unless he or she formally waives that right.

- Exceptions to the 10% early withdrawal penalty are available only in an IRA.

Disadvantages

- Can’t borrow against money in an IRA the way you can with many 401(k) plans.

Before making your decision, be sure to compare the underlying costs in your current or future 401k with those of an IRA. Be aware that costs vary widely among these vehicles.

In an era when most will retire without a pension, accumulating enough of a retirement nest egg to live comfortably is a challenge. As the chart illustrates, early and regular savings programs are critical because they capitalize on the positive impact of compounding. Consolidating retirement assets also improves your ability to create and maintain a coherent investment strategy, making the goal of a successful retirement more attainable.