I just celebrated a milestone birthday. I can no longer check the 50-59 box on surveys and forms. That’s right the big 6-0. Honestly, I had some trouble embracing this birthday. Keith Richards said, “No one wants to get old, but no one wants to die young.” That just about sums it up.

My birthday was a time of reflection, and a time to take stock. Was I where I wanted to be? I still haven’t lost those pesky 10 pounds. My basement and garage are still disorganized.

On the other hand, I do have a house, a wonderful husband and 3 great kids (4 if you include my son-in-law), a rescue dog, and some incredible friends.

But what about my financial life? I realized I needed a financial checkup along with my annual physical this year.

The following questions came to mind:

Retirement

When do I want to retire? When can I retire? Where do we want to live in retirement?

My milestone birthday prompted my husband and me to reflect on some places outside of Connecticut that we have visited recently and contemplate whether we might consider relocating in retirement. Nothing was decided but we agreed on a few more places to try out in the coming years.

How do I know if I am saving enough for retirement?

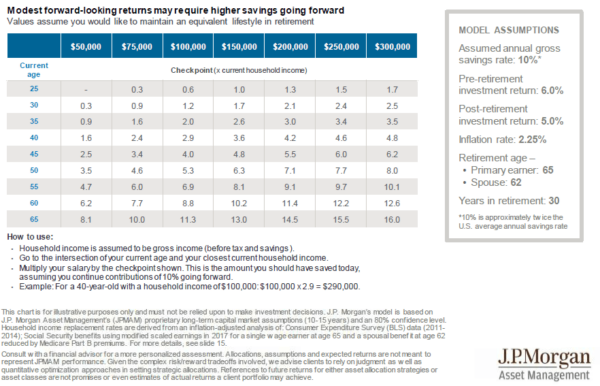

I used the chart from JP Morgan below as a guide and consulted with my advisor.

My husband and I realized if we did not increase our savings a bit now, we would need to find a way to spend less in retirement. I increased the amount I am contributing to my 401(k) each month and encouraged my husband to do the same.

We also checked on our investment allocation. Our advisor helped us to determine that a 65% appreciation/35% preservation target is right for our goals and needs. We took the time to make sure our accounts are close to target. We don’t want to expose our portfolio to undue risk.

I also took the time to get updated social security statements, check my work record and estimated benefit. You can do the same at ssa.gov.

Insurance

How much life insurance do my husband and I still need? Plenty on him- I would be so sad if he were gone; shopping might help. Is our long-term disability keeping up with our current salaries? Should we be buying long-term care insurance? Can we even afford it?

We reevaluated our life insurance. Now that we are closer to retirement, we decided to buy new term policies with reduced death benefits and lower premiums. We are now reviewing long-term care (LTC) policies and hope to redirect the premium savings from our life insurance to LTC.

While we are still covered by employer health insurance, we are taking the time now to understand Medicare so when the time comes, we will be better informed.

Estate planning

Should we meet with our lawyer to review and update our wills? Do we have power of attorney for each other if necessary? What do our health proxies say? Now that one of our daughters is married do we need to update the beneficiary information on our retirement accounts?

Shockingly, I was able to quickly locate our wills and realized that they haven’t been reviewed or updated in 20 years! I called our attorney and scheduled a meeting.

Budget review

I know an important factor in living comfortably in retirement is to be sure to live within your means. In order to prepare a realistic retirement budget, we need to first understand our current expenses, including housing costs.

We have made half-hearted efforts to budget in recent years, but have now committed to using the spending feature on our personal financial website to track our expenses in earnest. We are not done tracking yet, but it seems like we eat and drink a lot, and one of us visits the nail salon quite often.

The second piece of the expense equation is housing. If relocating is not in the cards, can we afford to stay in our home? To begin to answer this question, we need to get a handle on what our house actually costs us. We used a spreadsheet my advisor provided which includes not only mortgage and insurance costs, but also maintenance and long-term improvements. (For more on affording your house in retirement, read our blog What Does Your House Really Cost and Can You Afford it in Retirement?)

Although 60 seems like a big number, I think and hope that I have plenty of time to get my financial life in order and will eventually pass my financial checkup. To keep on task, I have put a “state of the financial union” meeting on the calendar for January- adult refreshments will be provided.