If you’re 70½ or older and still writing personal checks to charity, you may be leaving a significant tax benefit on the table. A Qualified Charitable Distribution (QCD) lets your IRA do the giving — and keeps the tax savings for you.

Advisor Joseph Donaldson breaks down how QCDs work, who qualifies, and the common mistakes that can disqualify your donation.

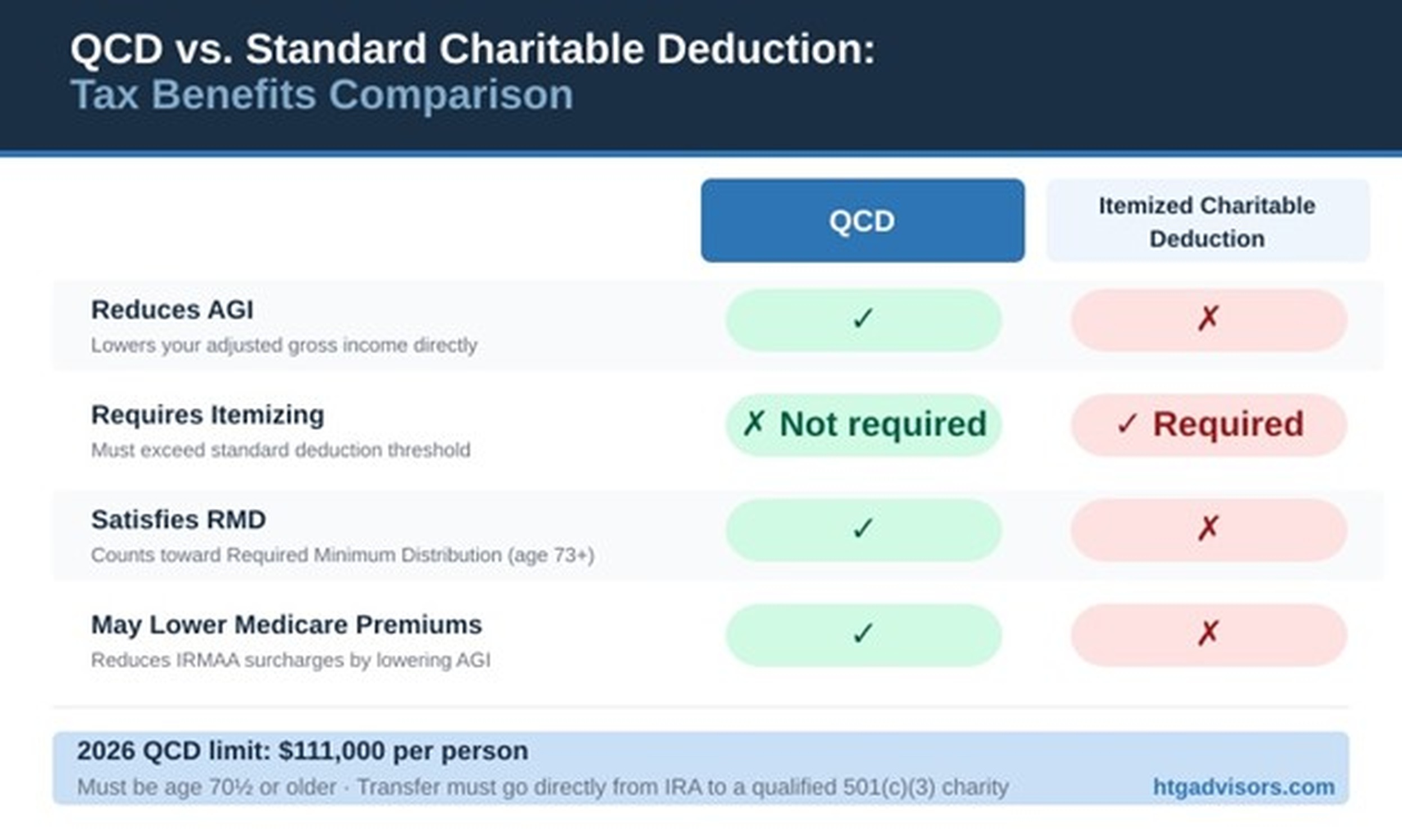

An IRA charitable rollover — formally known as a Qualified Charitable Distribution or QCD — is a direct transfer from your traditional IRA to a qualified 501(c)(3) charity. Unlike a standard charitable deduction, a QCD reduces your adjusted gross income (AGI) rather than sitting below the line as an itemized deduction. That distinction matters: a lower AGI can reduce taxes on your Social Security benefits, help you avoid or minimize Medicare IRMAA surcharges, and keep you in a lower tax bracket — all without needing to itemize.

Table of Contents

- What is a Qualified Charitable Distribution (QCD)?

- How QCDs Lower AGI and Reduce Taxes

- 2026 QCD Rules and Eligibility Requirements

- Common QCD Mistakes That Disqualify Your Donation

What is a Qualified Charitable Distribution (QCD)?

A QCD (also called an IRA charitable rollover) is a tax-free transfer from your traditional IRA directly to a qualified 501(c)(3) charity.

Key Requirements:

- Must be 70½ years old or older at time of distribution

- Transferred directly from IRA to charity

- Up to $111,000 per person annually (2026)

- Counts toward your Required Minimum Distribution (RMD) if account owner is 73 years of age or older.

How QCDs Lower Adjusted Gross Income (AGI) and Reduce Taxes

Qualified Charitable Distributions offer unique tax advantages because they reduce your AGI rather than providing a standard below-the-line itemized deduction. This IRA donation tax strategy creates multiple financial benefits:

Direct Tax Savings:

- Exclude up to $111,000 from taxable income with your QCD.

- Benefit even if you take the standard deduction (no need to itemize.)

- Satisfy your Required Minimum Distribution (RMD) without increasing taxable income (only if 73 years of age or older.)

Additional Financial Benefits:

- Avoid or reduce Income -related Medicare premiums (IRMAA) surcharges by lowering your AGI.

- Reduce taxes on Social Security benefits.

- Stay in lower tax brackets with strategic charitable giving.

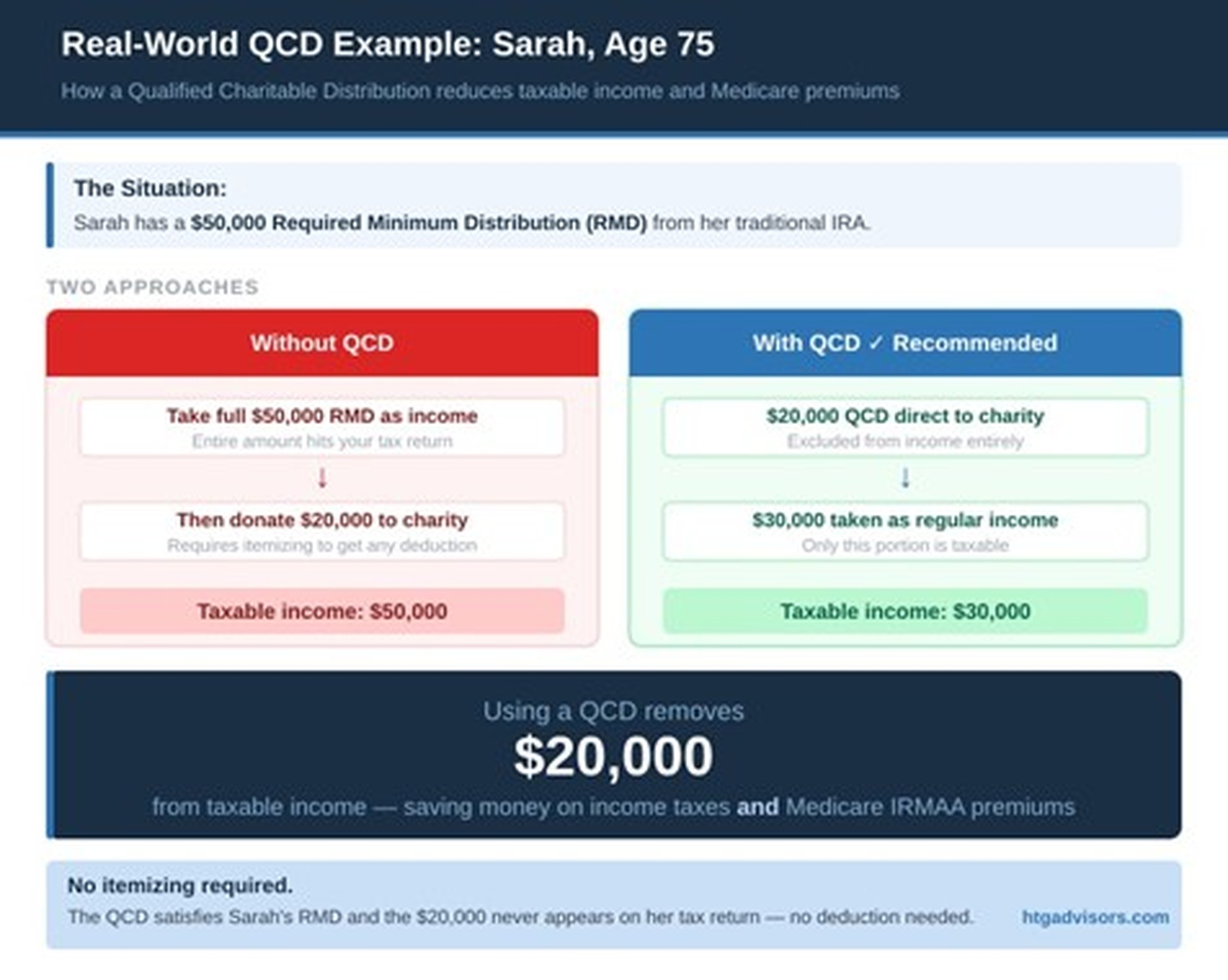

A real-world example illustrates how a QCD can reduce taxable income and Medicare premiums:

2026 QCD Rules and Eligibility Requirements

Before making an IRA charitable donation, ensure you meet these qualified charitable distribution requirements:

Age requirement for QCD eligibility: Must be exactly 70½ years old on the distribution date (not just “in the year” you turn 70½)

2026 QCD annual limits:

- $111,000 maximum per person for tax-free IRA donations

- Married couples: Each spouse can donate $111,000 from their own IRA (IRA charitable rollover limit applies per person.)

Qualified charities for QCD donations:

- Must be a 501(c)(3) organization: You can verify charity eligibility here.

- NOT donor-advised funds or private foundations (these don’t qualify for IRA charitable rollovers)

Important: If you made deductible IRA contributions after age 70½, your QCD exclusion reduces dollar-for-dollar.

Common QCD Mistakes That Disqualify Your Donation

Avoid these frequent errors that can disqualify your qualified charitable distribution or create unexpected tax bills:

- Wrong age calculation

You must be 70½ on the distribution date, not just in that year, e.g., if you turn 70 ½ on Wednesday, December 30th, you have two days to make the QCD. - Wrong account type for IRA charitable rollover

Use traditional IRAs only for QCDs. Roll 401(k)s to an IRA first to make a qualified charitable distribution. Failure to use the proper account could subject you to unexpected taxes. However, a beneficiary of an Inherited IRA, who is 70 ½ or older can make a QCD out of an Inherited IRA. While it may be possible to make a QCD from a Roth IRA, there is no advantage to doing so since Roth IRAs are already tax free when distributed (assuming all the qualifying rules are met). - Check payable to you instead of direct transfer

For a valid QCD, the check must be made payable to the charity—you cannot receive the funds first and then donate them to the charity This is a critical QCD process requirement. - Missing QCD documentation requirements

Get written acknowledgment from the charity before filing taxes. The IRS requires proper documentation for all qualified charitable distributions over $250. You must also receive acknowledgement of the gift and certify that no goods/services were provided in exchange for the gift. The receipt must be in hand before the donor files their tax return (no receipt => no QCD => no deduction). See “Substantiation Requirements” in IRS Publication 526 for further information. - Spouse limit confusion

Each spouse has their own $111,000 limit (2026) from their own IRA and are 70 ½ years of age—one spouse can’t donate $222,000. - Receiving goods or services in exchange

The QCD must be a pure charitable gift with no reciprocal benefit. If the IRA owner receives anything of value in exchange for the donation, the entire gift will not qualify as a QCD. Refer to IRS rules for limited exceptions regarding nominal goods or services that may be allowed. - Ineligible charities

Donor-advised funds and private foundations don’t qualify. The charity receiving the contribution must be a legal tax-deductible 501(c)(3) organization as defined by the IRS. Also, the account owner must receive acknowledgement of the contribution by the charity. - Not telling your tax preparer

Inform your tax professional of QCDs made during the tax year. For the 2025 tax year, the IRS created a new reporting code (Code Y) on Form 1099-R Box 7 to designate IRA charitable donations as Qualified Charitable Distributions. While custodians may use this code—often combined with code 7 or 4—to flag direct transfers to qualified charities, it remains optional for financial institutions for the 2025 tax year. - Making IRA contributions

If an IRA owner has made any deductible IRA contributions in or after the year of reaching age 70 ½, the QCD income exclusion to which they otherwise would be entitled is reduced, dollar for dollar, by the amount of those deductible contributions.

Ready to Reduce Taxes With an IRA Charitable Donation?

The HTG team helps retirees implement effective qualified charitable distribution strategies to maximize tax benefits.

Our professionals, including CERTIFIED FINANCIAL PLANNERS®, can help you:

- Determine if a QCD fits your retirement tax strategy

- Calculate optimal IRA charitable donation amounts

- Navigate QCD documentation requirements

- Facilitate qualified charitable distributions with your custodian

- Advise proper tax documentation for your QCD

Schedule a Free Consultation

A Qualified Charitable Distribution is one of the most powerful — and most underused — tax strategies available to retirees. If you’re 70½ or older, charitably inclined, and taking RMDs, a QCD may allow you to give more, keep more, and reduce your Medicare costs at the same time. The rules are straightforward, but the details matter — including the age calculation, the documentation requirements, and how a QCD interacts with your broader retirement income picture.

Have questions about whether a QCD fits your retirement tax strategy? Reach out to our team — we’re here to help you make the most of every charitable dollar.