A recession, which is a decline in economic activity, brings to mind companies going bust and employees losing their jobs. While there may have been as many as 48 U.S. recessions dating as far back as the Articles of Confederation, there have been seven over the past fifty years:

- The most recent one was also the shortest, lasting only two months as the world stopped to slow the spread of the Covid-19 virus.

- The longest was from December 2007 to June 2009 driven by a banking crisis and highly leveraged real estate. Commonly referred to as “The Great Recession”, the U.S. economy shrunk by 5% as measured by our Gross Domestic Product (“GDP”).

- The smallest decline in GDP, 0.3%, was in 2001.

Each has been different and there will be others. Economies go through cycles with expansions leading to contractions leading to the next cycle. Governments and central banks strive to mitigate the extremes. They provide stimulus in downturns and the reverse to cool an overheated economy. These efforts have never been able to eliminate the cycle entirely. In good times, consumers and businesses tend to overspend and overinvest. Then they cut spending excessively, fearing the contraction will be deeper and last longer than in the past.

Recessions don’t impact all employees equally.

Employees in businesses that are particularly sensitive to economic activity will be most at risk in a recession. As revenues drop, those businesses may cut employment to preserve profit margins. More stable or profitable businesses often choose to maintain staff levels, particularly if they perceive the downturn to be brief or if the labor market is tight.

And some benefit from a recession!

Recessions often lead to less inflation. The real estate market shifts to a buyers’ market in homes. More goods go on sale. My son loves Papaya King on Third and 86th St in New York City. During the ’08 recession, their “Recession Special” was 2 hot dogs and a medium papaya juice for $4.45.

Are we entering a recession?

The better question is when, not if, we will enter a recession. As a natural part of economic cycles, there will be a recession in our future.

With the current demand for goods and services greater than supply and more job openings than workers seeking employment, it is unlikely that a recession is imminent. The Federal Reserve expects inflation to moderate without the economy significantly contracting. Yet, balancing inflation and economic growth is never easy.

Are bear markets and recessions the same?

Recessions are defined by downward changes in economic growth. The term “bear or bull” market describes changes in the value of financial markets. While economic growth and how the stock market values businesses are related, they are driven by different factors. Stock markets fluctuate more than changes in the GDP.

When a financial market drops by more than 20% from its recent peak, it is referred to as a “bear market”. Drops of less than 20% are called “corrections.” The rest of the time, which is most of the time, it is a “bull market.”

There have been five bear markets in the last fifty years and seven recessions. Some of the market drops occurred ahead of the start of a recession, while others happened at the same time. There was a bear market in October 1987 without an associated recession, and recessions can occur without bear markets.

A stock market drop can be the result of a variety of factors:

- Lower projected earnings per share across many companies and sectors.

- A return to rational valuation levels after a period of excessive investor enthusiasm.

- Higher interest rates leading to a lower present value of future earnings.

- A shock to the system, such as a pandemic, a terrorist attack, or war.

- Other factors such as a change in taxation, regulation, competition, or currency fluctuations.

Bear markets and recessions have different impacts

A recession is worrisome for all who are impacted by declines in business activity. Less activity may lead to lower profits for business owners and less employment for workers. Investors experience stress during bear markets as the value of their savings declines, causing an increased concern of having to sell stocks before the market recovers.

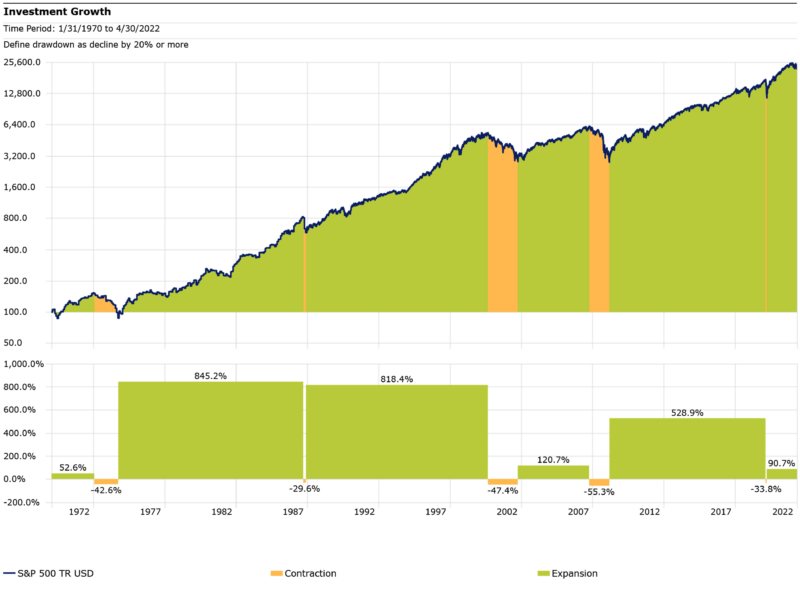

As illustrated in the following graph, most of the time the stock market returns to its previous peak within five years. Once in the last fifty years, it took ten years. The blue line is the value of the S&P 500 Index of U.S. stocks since 1970. Orange shaded periods are bear markets where the Index dropped by more than 20%. Green shaded periods are the periods of market appreciation, “bull markets”, in between each drop. While the “bulls” last longer than the “bears”, there is no pattern as to when one ends and the next starts.

Should you change your investment strategy now?

As we publish this blog at the beginning of June 2022, the S&P 500 Index of U.S. stocks is at 4,000, down 17% from its peak of 4,800. No one knows whether there is more of a drop to go, or if this is close to the start of a period of market appreciation. However, we do know that a tactical shift out of equity markets too early or too late leads to poor long-term investment returns.

The lesson of past economic and stock market cycles is that long-term investors are not hurt by recessions or bear markets if they have an appropriately designed portfolio strategy and remain invested in accordance with that strategy.

Rather than guessing at timing, it is best to use the volatility of financial markets to your advantage:

- Maintain your overall level of risk through rebalancing: trimming the winners and adding to quality investments at attractive prices.

- Have sufficient low-volatile assets to meet your spending needs while stock markets are down.

- Use the volatility to save taxes through the technique of “tax loss harvesting” in your taxable accounts.

Maintaining a portfolio’s risk commensurate with your needs and goals will insulate your wealth from recessions and provide much greater peace of mind.