Inherited IRA rules have become increasingly complex with the SECURE Act and SECURE 2.0. New requirements took effect in 2025 that can dramatically impact beneficiaries’ tax situations.

Inheriting a retirement account should feel like a gift—but for many beneficiaries, complex and ever-changing IRS rules turn that gift into a source of stress and costly mistakes. If you’ve inherited an IRA or are planning your estate with loved ones in mind, it’s important to understand the new requirements. CERTIFIED FINANCIAL PLANNER® certificant Allison Donaldson has compiled this guide to help you navigate these changes.

Table of Contents

What is an Inherited IRA, and Why Do They Matter?

What Are the Basic Inherited IRA Distribution Rules now?

Who Qualifies as an Eligible Designated Beneficiary?

What Is the 10-Year Rule for Inherited IRAs?

How Do I Calculate My Required Minimum Distribution from an Inherited IRA?

What Tax Planning Strategies Should I Consider for Inherited IRA Distributions?

What Happens If I Miss an Inherited IRA Required Distribution?

How Does Inheriting a Roth IRA Differ from a Traditional IRA?

What Should I Know About Inherited IRAs and Estate Planning?

What is an Inherited IRA?

An inherited IRA—also called a beneficiary IRA—is a retirement account you receive as a beneficiary when the original owner passes away. It can be either a traditional IRA (pre-tax contributions, taxable distributions) or a Roth IRA (after-tax contributions, tax-free distributions). Unlike your own IRA, you cannot make additional contributions; you can only take distributions according to IRS rules and timelines, which depend on your relationship to the deceased and when they passed away.

What Are the Basic Inherited IRA Distribution Rules now?

The inherited IRA landscape changed dramatically with the SECURE Act of 2019 and subsequent SECURE 2.0 legislation. For IRAs inherited after December 31, 2019, most non-spouse beneficiaries must withdraw the entire balance within 10 years of the original owner’s death—ending the previous “stretch IRA” strategy.

Starting in 2025, the IRS finalized regulations requiring certain beneficiaries to take annual required minimum distributions (RMDs) during the 10-year period. Your specific rules depend on:

- your relationship to the deceased account owner,

- whether the original owner had reached their Required Beginning Date (RBD) for RMDs, and

- when the account owner passed away.

Pro Tip: Keep detailed records of when you inherited the IRA, whether the original owner had started taking RMDs and if the original owner satisfied their current year RMD before death. This documentation will be critical for determining which distribution rules apply to your situation.

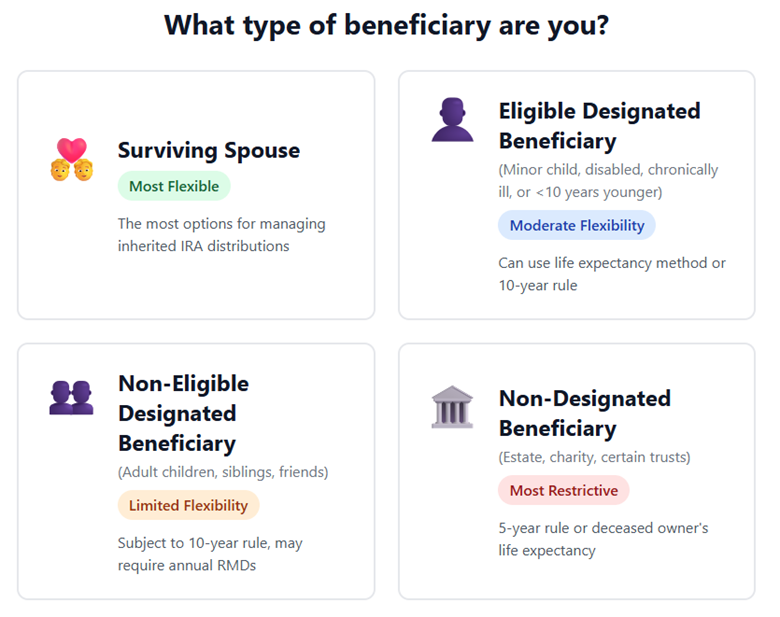

Who Qualifies as an Eligible Designated Beneficiary?

An Eligible Designated Beneficiary (EDB) receives preferential tax treatment under the SECURE Act, allowing them to stretch distributions over their lifetime using the life expectancy method rather than emptying the account within 10 years.

EDBs include:

- Surviving spouse of the account owner

- Minor children of the account owner (until reaching the age of majority)

- Disabled individuals as defined by IRS standards

- Chronically ill individuals meeting specific criteria

- Individuals not more than 10 years younger than the account owner

- Certain qualified trusts established for the benefit of eligible beneficiaries

Surviving spouses can treat the account as their own, roll it into an existing IRA, or take life expectancy-based distributions.

Pro Tip: If you’re an eligible designated beneficiary, consult with a financial advisor to evaluate whether the life expectancy method or the 10-year rule provides better tax outcomes for your specific situation.

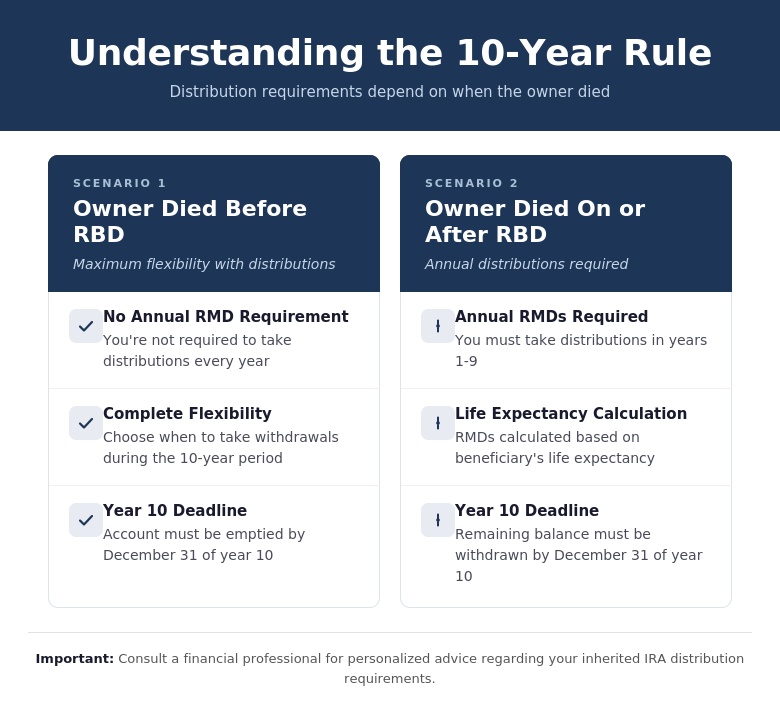

What Is the 10-Year Rule for Inherited IRAs?

The 10-year rule requires non-eligible designated beneficiaries to fully distribute the inherited IRA by December 31 of the tenth year following the owner’s death—applying to most adult children, siblings, friends, and other non-spouse beneficiaries who inherited IRAs after 2019.

The critical 2025 update: if the original owner had already begun RMDs at death, beneficiaries must take annual RMDs in years 1–9 and still empty the account by year 10. If the owner died before their RBD, no annual distributions are required, but the account must be depleted by year 10.

This distinction creates two different scenarios:

Pro Tip: Missing required RMDs can trigger IRS penalties of up to 25% of the amount that should have been withdrawn. Mark your calendar for December 31 deadlines and consider setting up automatic distributions to ensure compliance.

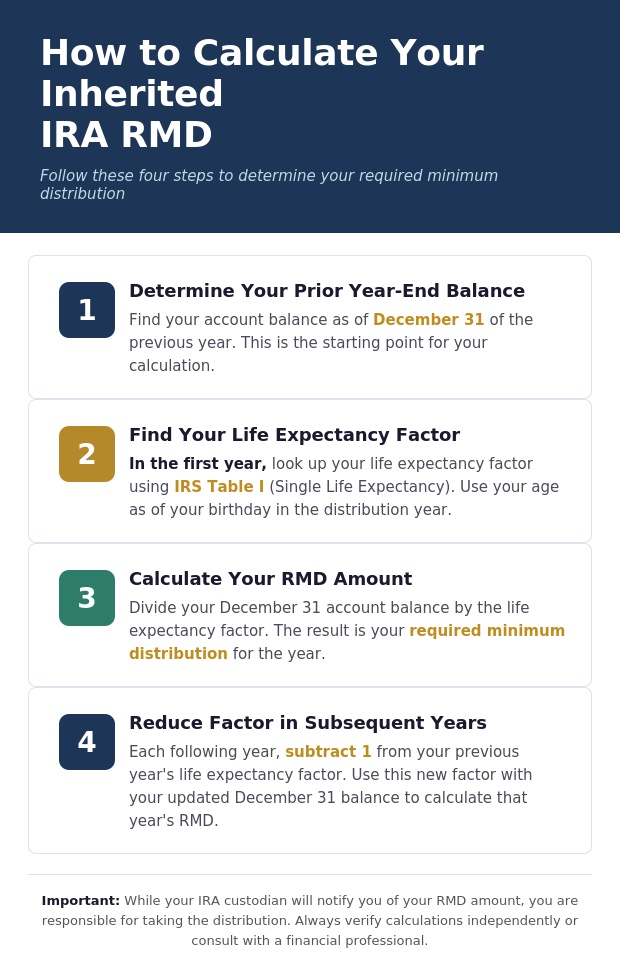

How Do I Calculate My Required Minimum Distribution from an Inherited IRA?

Calculating inherited IRA RMDs requires knowing which life expectancy table to use and applying it to your account balance. For non-eligible designated beneficiaries subject to annual RMDs, the calculation follows these steps:

The IRS provides detailed guidance in Publication 590-B. Many IRA custodians also offer RMD calculators—Fidelity’s inherited IRA RMD resource and Schwab’s Inherited IRA RMD Calculator can simplify this process.

Pro Tip: Your IRA custodian is required to notify you of your RMD amount each year, but the responsibility for taking the distribution rests with you. Verify the calculation independently or work with a professional.

What Tax Planning Strategies Should I Consider for Inherited IRA Distributions?

Strategic planning can significantly reduce your tax burden. The key is avoiding a large lump-sum distribution in year 10 that could push you into higher tax brackets.

Consider these tax-efficient strategies:

- Bracket Filling Strategy Take annual distributions that fill your current marginal income bracket without pushing into the next, spreading tax liability across multiple years at lower rates.

- Timing Based on Income Fluctuations If you anticipate years with lower income—such as gaps between jobs, early retirement years, or sabbaticals—take larger distributions when your marginal tax rate is lower.

- Extend tax-deferred growth Take distributions from an inherited IRA and contribute up to the annual maximum to your own IRA, Roth IRA, or qualified retirement plan (if eligible) — so you can continue building tax-advantaged savings with the same dollars.

- Charitable Giving Integration Coordinate larger distributions with years of significant charitable giving, so deductions offset the added taxable income.

- State Tax Planning If planning to relocate to a no- or low-income-tax state, defer larger distributions until after your move.

Pro Tip: Work with a financial or tax professional to run projections for multiple distribution scenarios before deciding on your strategy. Consider factors like future Social Security taxation, Medicare premium surcharges (IRMAA), and potential loss of tax credits or deductions.

What Happens If I Miss an Inherited IRA Required Distribution?

Missing a required distribution triggers a penalty of up to 25% of the RMD amount, reducible to 10% if you correct the error and file IRS Form 5329 promptly. The IRS waived penalties for missed RMDs from accounts inherited in 2020–2023, but those waivers ended in 2025—compliance is now fully required.

If you discover you’ve missed an RMD:

- Take the missed distribution as soon as possible

- File Form 5329 with your tax return

- Request a waiver of the penalty by providing reasonable cause

- Keep documentation of your corrective actions

Pro Tip: If you discover you’ve missed an RMD, act immediately. The sooner you take the missed distribution and file Form 5329 requesting a penalty waiver with reasonable cause, the better your chances of IRS approval. Document everything, including when you discovered the error and the steps you took to correct it.

How Does Inheriting a Roth IRA Differ from a Traditional IRA?

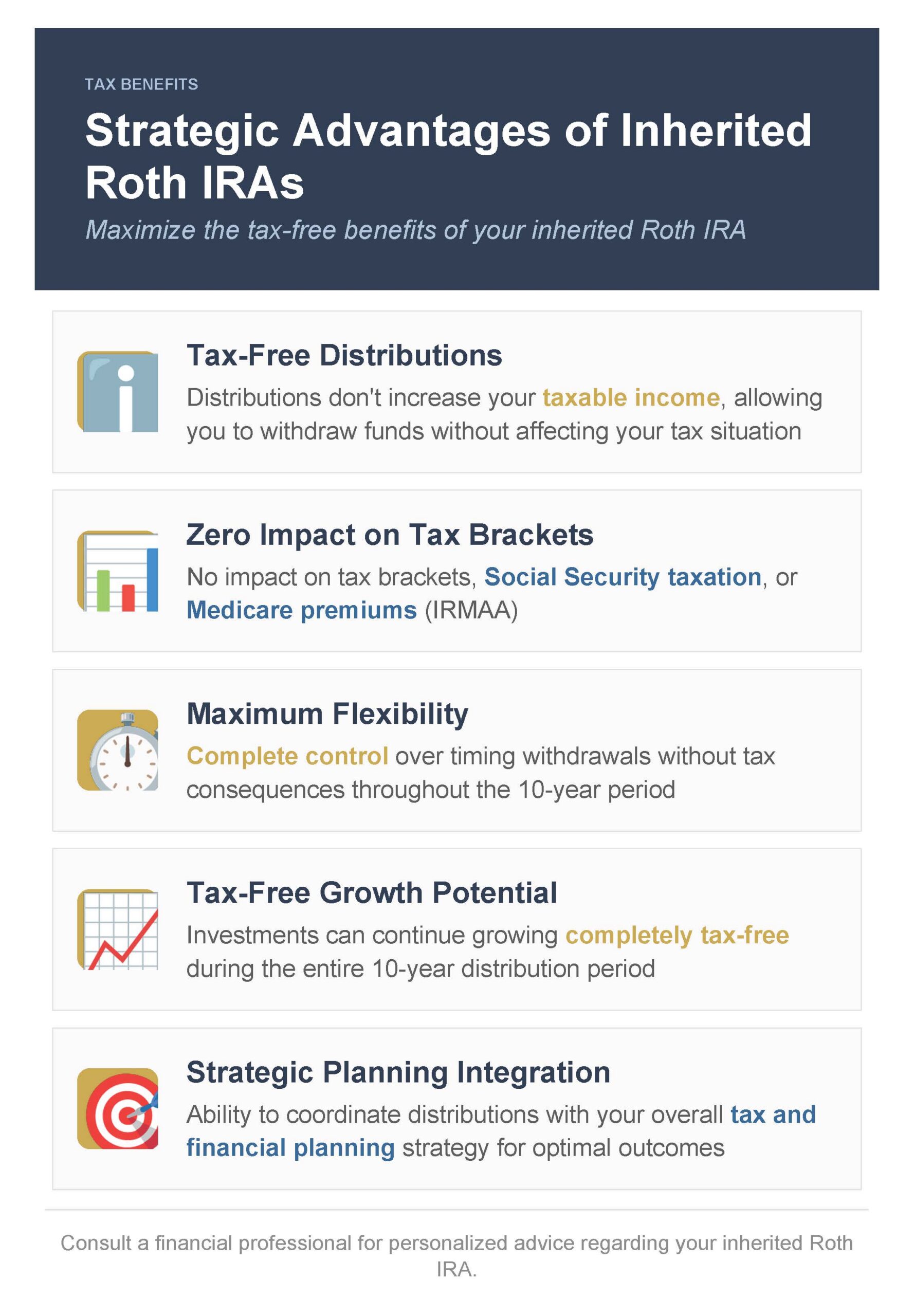

While Roth and traditional inherited IRAs both follow the 10-year distribution timeline for most beneficiaries, the tax treatment differs significantly. Inherited Roth IRA distributions are generally tax-free, provided the original account was open for at least five years before the owner’s death.

A Key Roth IRA Advantage: No Annual RMDs

Unlike traditional IRAs, Roth IRA owners never take RMDs during their lifetime, so all are treated as having died before their RBD. Non-eligible designated beneficiaries of Roth IRAs do NOT have to take annual RMDs during the 10-year period—they only need to empty the account by December 31 of the tenth year. Because no annual distributions are required, assets keep growing tax-free for up to ten years, and distributions remain tax-free (assuming the five-year rule is met).

This creates tremendous flexibility. You can:

- Take no distributions for nine years and withdraw everything in year 10

- Take distributions in any year(s) you choose

- Withdraw the entire balance in year one

- Take strategic distributions

Strategic Advantages of Inherited Roth IRAs:

Surviving spouses can treat the account as their own, eliminating RMD requirements entirely during their lifetime and allowing tax-free growth for potentially decades longer.

Pro Tip: If you don’t need the funds for living expenses, delay distributions as long as possible within the 10-year window to maximize tax-free growth. Since distributions are tax-free, a year-10 lump sum doesn’t create the same tax concerns as traditional IRAs—just don’t miss the deadline.

What Should I Know About Inherited IRAs and Estate Planning?

The elimination of the stretch IRA strategy has significant estate planning implications.

- Beneficiary Designation Review Designations override your will—review them regularly to ensure alignment with the new rules and your estate planning goals.

- Qualified Trusts as Beneficiaries Naming a trust as an IRA beneficiary can provide control and asset protection, but requires careful drafting to qualify as a “see-through” trust—improperly structured trusts trigger even less favorable distribution rules.

- Charitable Beneficiary Strategy Since charities aren’t subject to income tax, naming a charity as an IRA beneficiary while leaving other taxable assets to individual heirs is highly tax-efficient—charities receive the full IRA value without tax erosion.

- Multiple Beneficiary Considerations With multiple beneficiaries, the least flexible category determines the rules for all—unless separate accounts are established by December 31 of the year following death.

- Tax Impact on Beneficiaries Consider each beneficiary’s tax bracket when designating IRA heirs, as high-bracket beneficiaries may face a significant tax burden.

Pro Tip: Schedule a comprehensive review of your beneficiary designations with an estate planning attorney and financial advisor at least every three to five years, or after major life events. Ensure your designations align with current tax laws and your overall estate planning objectives. Don’t forget to name contingent beneficiaries in case primary beneficiaries predecease you.

How Can Professional Guidance Help with Inherited IRA Complexity?

With significant financial consequences for mistakes or missed opportunities, professional guidance offers several advantages:

- Tax Planning Expertise Tax planning professionals model distribution scenarios and help minimize tax liability across the 10-year period.

- Coordination with Overall Financial Plan Inherited IRA distributions should fit your income needs, retirement timeline, other investment accounts, and long-term goals.

- Compliance Assurance Professionals stay current with evolving IRS guidance, ensuring you meet all RMD requirements and avoid costly penalties.

- Estate Planning Integration Advisors can structure beneficiary designations to maximize tax efficiency. HTG’s estate financial planning services can help ensure your retirement accounts are integrated into your overall wealth transfer strategy.

- Life Event Adaptation As your circumstances change—marriage, divorce, retirement, career changes, or major purchases—professionals help adjust your inherited IRA strategy to fit your new circumstances.

The 2025 finalized regulations mark a turning point for inherited IRA beneficiaries. Whether you’ve recently inherited an IRA, expect to in the future, or are structuring your own estate, understanding your beneficiary status, RMD obligations, and 10-year distribution requirements isn’t optional—it’s the difference between a smart financial decision and a costly mistake.

At HTG Advisors, we help clients navigate exactly these situations. Our approach integrates inherited IRA distributions into your broader tax strategy, retirement plan, and long-term financial goals so you’re not just staying compliant—you’re making the most of what you’ve inherited.

The rules are complex, but your next step doesn’t have to be. Let’s build a strategy that protects your assets and minimizes your tax burden.