In Part 1: Key Considerations for Long-term Care, we explored some of the data surrounding long-term care (LTC) and the factors that might contribute to greater likelihood of needing care. In this blog, we take a step further and explore how to integrate this knowledge into your financial plan.

Testing your financial plan for an LTC need

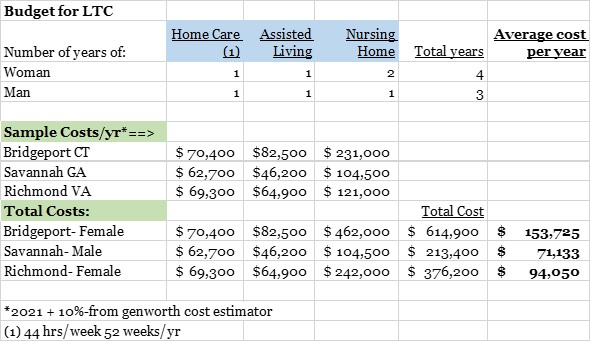

In the research done by the US Department of Health and Human Services (HHS), https://aspe.hhs.gov/reports/ltss-older-americans-risks-financing-2022, the amount of care for women was 3.6 years versus 2.5 for men. Using this information, we “test” your financial plan by modeling a long-term care need that is slightly worse than average – three years for men and four years for women.

Rather that assuming that care will all be provided in a nursing home setting, we use the research which shows that most often care is provided in a continuum of intensity from periodic assistance to round the clock care. We break down the type of care as follows:

While the research shows that many receive unpaid care at home for some portion of the time, we assume all care requires payment.

What does LTC cost?

The next step is to quantify what care might cost. Where can you find such data? You can start by going to your State Dept on Aging (directory can be found here: https://www.hhs.gov/aging/state-resources/index.html.)

In addition, Genworth, a major LTC insurer, publishes data on LTC costs across the country annually, and these costs can be found on their website: https://www.genworth.com/aging-and-you/finances/cost-of-care.html.

Using the Genworth data (from 2021) and updating for recent inflation, we develop an estimate of total potential costs you might face, given your location, and adjust for any family health history.

For example:

The information contained above is for illustrative purposes only

By taking an objective, data-driven approach, we can focus on what costs are reasonably probable and not engage in either wishful thinking or exceedingly unlikely worst-case scenarios.

How to manage the risk of needing long-term care? That is the question!

There are several ways to manage and mitigate the risk of needing care for an extended period.

- Some may choose to rely on family members to care for them, at least at the outset. One thing that is changing and may not be fully reflected in the research is that as everyone lives longer, married couples may find that even if spouses are willing to care for each other, they may not be able to due to their own frailty. While it might have been feasible for a 70-year-old to care for a 75-year-old spouse years ago, it isn’t as feasible for an 85-year-old to care for a 90-year-old.

- Another way to handle the risk is to move into a life care community where different levels of care are offered. The financial arrangements in these communities vary widely, making it impossible to summarize these arrangements easily. Some involve a large deposit and protect you from significant increases in monthly charges in the event you need care, essentially locking your monthly costs no matter your LTC need. Others charge more as you need more services. It is important to investigate what you will be charged if your needs increase.

- A third way to mitigate the financial risk of needing care is to consider purchasing long-term care insurance. This area of insurance has undergone much change in the last 20 years. Policies purchased 20 years ago promised low premiums, but insurance companies underestimated how many claims they would face. They were also hurt by the extended period of low interest rates. The net result is that insurers have petitioned state insurance agencies to raise rates on existing policies. Even so, older policies are still a bargain for the benefits that can be received.

Many insurers left this part of the insurance market, and the number of companies offering LTC policies has dropped dramatically. New policies have been adjusted to reflect the fact mentioned earlier that a 65-year-old has a 56% chance of making a claim! As a result, policies are not nearly as affordable as they once were. The insurance industry has innovated a new type of policy as well. Called a “hybrid” policy, it blends LTC benefits with life insurance. If you are contemplating this solution, it is best to explore it as soon as possible, as policies get more expensive, and you are less likely to pass the medical underwriting as you age.

- The fourth way to is to self-insure by setting aside an amount that can cover your estimate of your needs or an estimate of the present value of your future needs. For many, their home might be the asset tapped at the end to cover LTC costs. The consequence of this route is that your heirs may inherit less.

Self-insuring is a viable route, but it should be discussed in the context of a full financial plan, considering the impact on a surviving spouse should one spouse fall ill. Consider also how you might feel about spending down your heirs’ inheritance.

- The last resort is to rely on Medicaid to pay the bill. Using Medicaid as a strategy requires you to either give away (well before you need care) all your assets or use them for your care. There are some exceptions if you are married, but the rules are not geared to allowing a couple to retain much while being eligible to receive Medicaid assistance.

The fact of the matter is that no one likes paying for LTC. However, including LTC in your financial plan is an important element in stress-testing your long-term plan to ensure you have adequately considered this more-than-likely event.