Saving is an essential ingredient to your financial health and future, but putting a plan in place to save can be challenging (and sticking with it even harder).

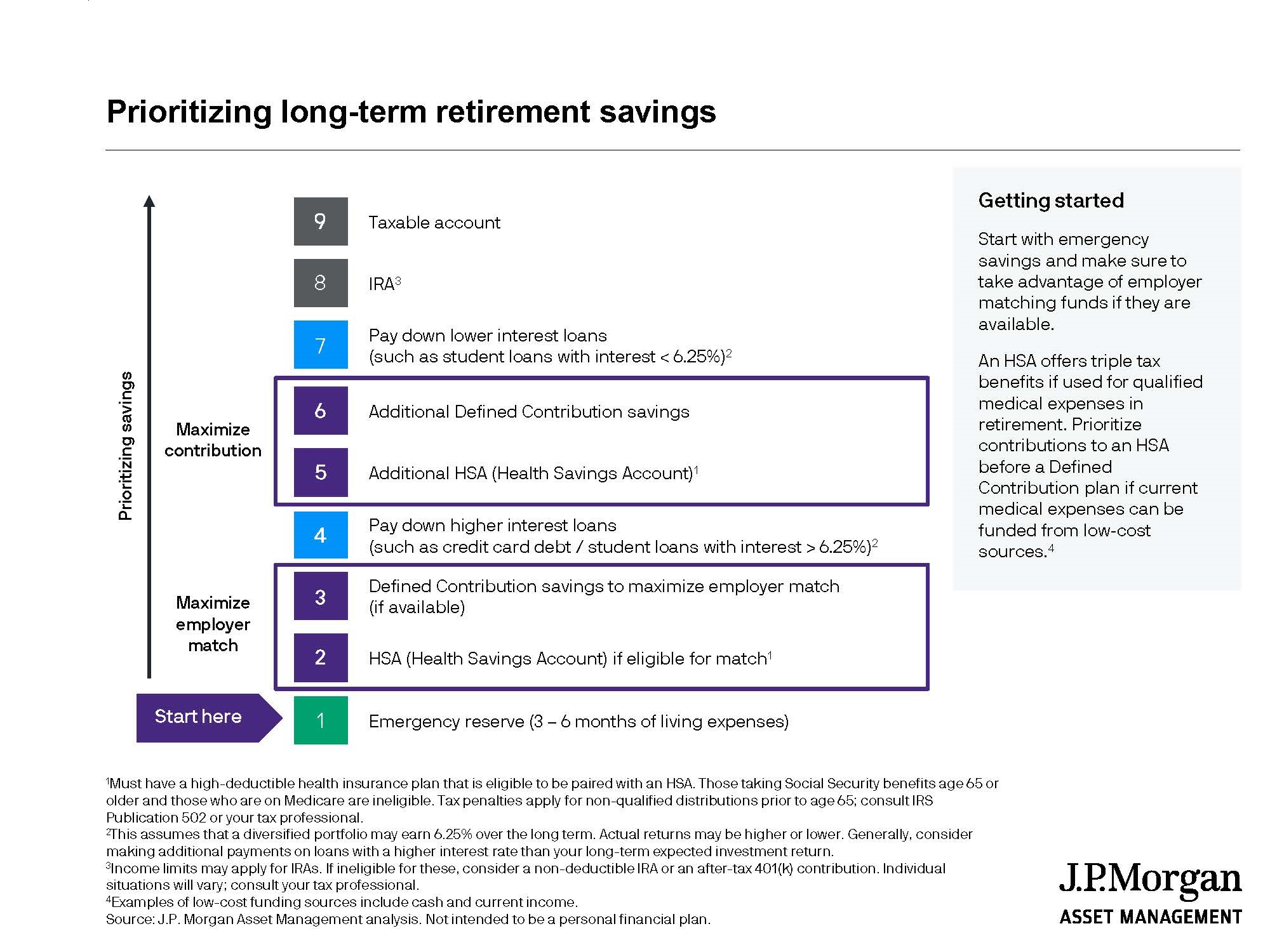

The graphic below outlines how you should prioritize savings and which accounts to fund first with your surplus cash.

Once you build up your emergency fund as a safety net, move on to utilizing tax-advantaged accounts (i.e., defined contribution plans like a 401(k), HSA) and paying down loans, especially high interest debt.

Did you know that by contributing pre-tax to a retirement plan, the lower your taxable income – and tax bill – will be?

Bonus to saving!

Next, move on to individual retirement accounts (IRA) and taxable accounts.

Now that you know where to save, how do you plan and implement your strategy? Here are some tips and tricks to follow.

50/30/20 Rule: Divide up your after-tax income and allocate 50% to needs, 30% to wants, and 20% to savings (or paying down high-interest debt). If your needs make up a larger portion, you will need to spend less on wants to ensure you hit your savings goals.

Create a budget: Take inventory of your fixed and variable expenses and establish a budget to track your spending. This will help pinpoint areas where you are spending too much and evaluate if you really want to be spending in this area or prioritize other things.

Create an auto-savings plan: Employer retirement plans like a 401(k) plan is a great place to start since a % of your salary gets deducted each paycheck towards retirement. Do you have additional surplus each month? Set up an automatic transfer on payday from your checking account into your savings or brokerage account.

Understand your debt: Monitor interest rates on existing debt and look for ways to restructure or pay it down. For example, credit cards come with high interest rates, so focus on paying this off each month. Do you own a home? If interest rates fall, look at refinancing your mortgage to pay less in interest.

Never borrow against your retirement: 401(k) plans can offer loans but only use these as a last resort for emergencies and not for living expenses. You are borrowing against your future self, and you are paying the pre-tax loan back with after-tax dollars. For example, if you took out a loan of $10,000 and your tax rate is 20%, you will pay more than $10,000 back to pay down the loan, since every $1 will get taxed and amount to $0.80 (20% taxed).

Reevaluate savings when you receive raise or bonus: If you receive a bonus and/or raise, look at earmarking a portion to your savings plan.

Take Action Now!

- Download a budgeting app (such as Mint or PocketGuard) to help get organized and set up a budget.

- Create your savings goals and implement an auto-savings plan.

- Schedule an annual review of savings – at least once a year take inventory of your savings goals and progress each year. Did you meet or exceed your goals? Are you in line with the 50/30/20 rule? If not, what were the reasons, and can you change your habits?

- Review annual savings needed if you start saving for retirement today!